How ESG is and will continue to shape property investment

The real estate industry is continuously adapting to the growing impact of ESG. This month, we dive headfirst into the results of our second ESG Property Investor Survey. This year’s results highlight the key drivers of ESG strategies, the financial and operational impacts of inaction, and a growing appetite for retrofitting. Complementing this, we conclude our Meeting the Commercial Retrofit Challenge series, our third report in the series provides actionable insights into the opportunities and challenges of upgrading assets.

03 April 2025

Value creation and preservation

ESG considerations remain firmly in property investment and operational strategies. That is the key message of our 2025 ESG Property Investor Survey. A year and a half has passed since our inaugural survey, over which time the landscape has become increasingly complex. Yet, the fundamental drivers of ESG remain clear to investors; risk identification, mitigation, and, ultimately, creating and preserving value.

When asked what the key driver of their ESG strategy is, 63% of the 40 investors we surveyed, who combined represent some £300 billion in assets under management, cited enhanced returns. Market forces will continue driving their implementation.

Nearly 70% of respondents cited internal net-zero goals as a key ESG strategy driver, this was most notable among larger investors. While disclosures play a role in transparency and may have initially advanced net-zero plans, internal ESG policies are reshaping procurement. A growing number of customers and investors are demanding sustainable and responsible practices, making net-zero policies essential for competitiveness – regardless of regulation or disclosure requirements.

The growing cost of inaction is also becoming evident. Over a quarter (28%) of respondents reported higher capital expenditure due to weather-related damage, while 34% noted increased operational expenditure from rising insurance premiums and energy costs. These are notable as they feed through to valuations. Additionally, there is a widening gap of rents for offices with lower efficiency credentials. We highlight in Part 2 of Meeting the Commercial Retrofit Challenge that rental levels of EPC C-rated offices have seen the gap relative to prime rental levels widen in recent years, to an average of 27%.

Retrofitting and refurbishing opportunities

Retrofitting and refurbishing existing assets has emerged as a primary ESG strategy, driven by financial incentives and the recognition of value opportunities, as pointed to recently by an ex-Goldman Sachs banker. According to the latest UN Global Status Report for Buildings and Construction, the rate of building energy efficiency retrofits must triple by 2030 to achieve a 35% reduction in energy intensity. While buildings have made progress in 2023, consuming 32% of global energy and contributing 34% of global emissions (down from 37% in 2022), the pace of action needs to quicken.

Property owners and investors have that burgeoning desire for retrofitting and refurbishing, yet action has been constrained by changing goalposts, high build and finance costs and, in some cases, skills shortages. Our three-part series on Meeting the Commercial Retrofit Challenge, looks to demystify those baselines with key considerations around sustainability, dependent on the occupier pool and targets.

Our survey confirms the intention with almost three-quarters of respondents identifying retrofitting existing assets as a primary ESG strategy for property - a figure that has held steady since our last survey in 2023. Importantly, it is not just about existing portfolios; the desire to acquire poor-ESG-performing assets to retrofit has grown. Some 62% cite this as a strategy, up from 58% in our previous survey. Yet, our survey indicates that the hurdle of acquiring opportunities may still exist as only 17% of investors want to dispose.

These strategies are not confined solely to offices. For example, Fidelity International have just raised $110 million for this strategy in the logistics sector across Europe. Furthermore, while restoring and repurposing historic buildings has its challenges, as previously highlighted, Historic England has been reviving high streets. The scheme, which repaired 723 historic buildings and restored 462 shopfronts, created 700 jobs valued at £34 million a year. According to Amion consulting, the scheme returned £1.34 for every £1 invested. Early research has also suggested increased footfall, which could magnify the benefits, although more research is needed. The project also only brought 224 homes back into use, falling well short of the 2,700 target, demonstrating the challenges.

Critical to realising opportunities is timing. There is a window of opportunity with a shortage of higher-sustainability assets (explored in the UK Cities DNA series) in many markets that is not set to ease. As projects can span years when accounting for feasibility, planning and construction – as we discuss in Part 3 - is crucial for asset owners to take stock and make plans for assets to ensure value is protected and enhanced.

Liquidity in markets

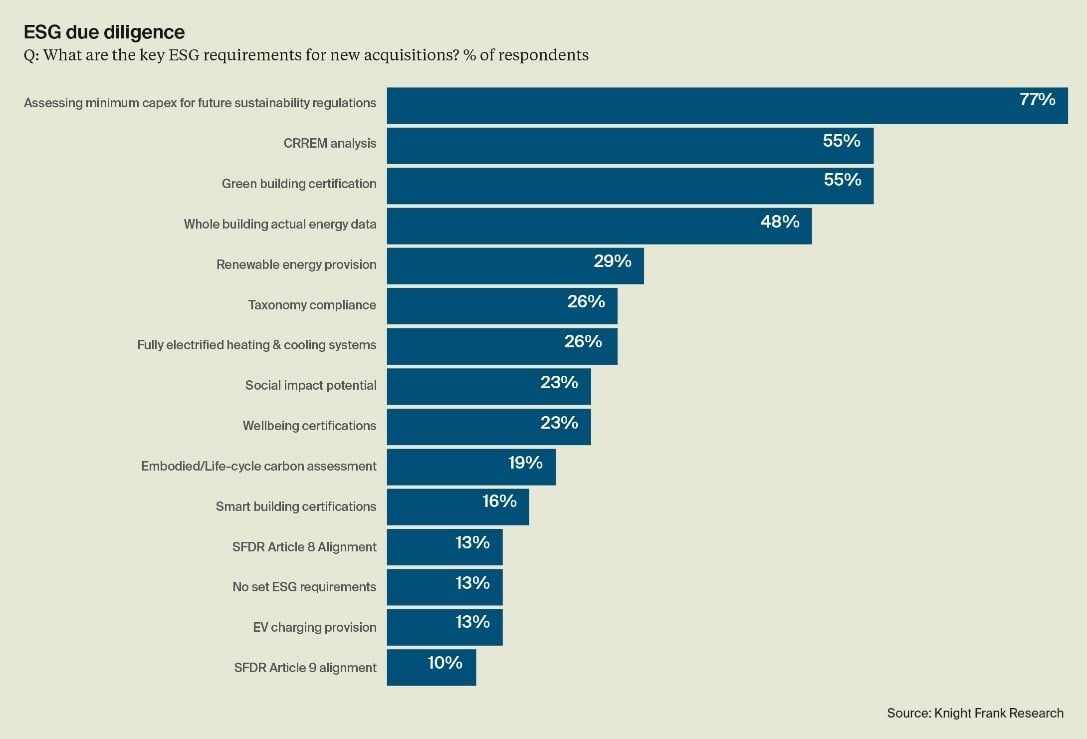

Understanding what is conducive to value is imperative when undertaking upgrades – demystifying the baseline. Our survey unearthed three key themes of how investors assess ESG: data, compliance and energy.

Accurate and verifiable data is essential for assessing building performance and risk. For example, more than half of the respondents use CRREM (Carbon Risk Real Estate Monitor) to understand building performance and risk; when looking at institutional funds 72% use CRREM. Some investors now set minimum CRREM stranding dates, avoiding assets nearing obsolescence or those where stranding comes before lease expiry. For asset owners ensuring accurate data capture will become more of a requirement.

Regulatory compliance is still a consideration. More than three-quarters assess the capex required to bring the asset into compliance with future or proposed regulations, such as the proposed minimum EPC B in England & Wales. In addition, a quarter of investors, and more than 40% of those with mainland European assets, look for EU Taxonomy compliance - which for retrofits means reducing the primary energy demand by 30%.

The source of energy is a growing focus. While 29% of investors require renewable energy provisions for new acquisitions, and 26% look for fully electrified heating and cooling systems, adoption of on-site renewable power remains limited across portfolios. Just shy of 60% reported that less than 10% of assets had some on-site provision. The UN Report highlights the need to triple the deployment of on-site renewables by 2030, with the total share of energy consumed from renewable sources rising to 46%. This shift could enhance asset appeal and provide additional revenue streams.

Meeting specific criteria – which the Institutional Investors Group seeks to clarify further - could broaden the pool of potential investors when looking to exit the asset, potentially boosting liquidity and value. See the full report here.

Nicola Ryan's stat of the month: 2%

The UK’s carbon emissions from commercial buildings remained flat in 2024, while emissions from all buildings rose by 2%, according to provisional data from the Department for Energy Security and Net Zero (DESNZ). This marks a step backwards, likely driven by increased gas use, and falls far short of the reductions needed to stay on track for net-zero by 2050. With buildings responsible for around a fifth of the total, accelerating energy-efficient retrofits remains critical. As ESG pressures grow, property owners must plan for decarbonising portfolios or risk obsolescence. Explore the full implications in our Meeting the Commercial Property Retrofit Challenge series.

What else I am reading

Planning and infrastructure bill included households seeing up to £2,500 off energy bills if living within half a km of new or upgraded power infrastructure; Adaptation will be a growing area for real estate, including homes, as extreme weather becomes more frequent; Circularity in retail is rising with second-hand sales globally climbing 15% in 2024, we previously looked at implications for physical stores and logistics; and a £60-a-month heat pump subscription? Conservative leader Kemi Badenoch states that net zero by 2050 is impossible; and Australia invests A$250 million in nature.

Sign up to Knight Frank Research.