The New Frontier - Your weekly science and innovation update

Your weekly pulse check on science and innovation. Those on the supply side of real estate can track the trends set to drive demand, while occupiers gain fresh perspective on competitor activity and sector dynamics.

01 December 2025

Signals from the conference room floor

Both London Life Sciences Week and the Jefferies Healthcare Conference delivered the same verdict. Life sciences is not a sector in retreat, but one grappling with patent expiries, a more selective funding environment, intensifying competition, greater volatility, pressure to increase sales while driving efficiency and a shifting geography of innovation. On the other hand, dry powder is increasing, policymakers continue to lean in, and the scientific frontier continues to widen.

At the Jefferies healthcare conference familiar themes resurfaced. Big pharma’s patent cliff is getting steeper. Across the next five years, large drugmakers are facing a patent expiry “wall” of roughly $236 billion of revenue and will need to replace the equivalent of 8–10 blockbuster franchises per year over the coming decade. This is structurally bullish for external innovation and M&A.

At the same time, dry powder remains substantial. Specialist investors and corporate venture arms still have capital to deploy, even if they are more discriminating than during the 2021 peak. Contract research organisations and life sciences tools companies continue to report solid earnings, which points to healthy underlying demand.

London Life Sciences Week added a more forward-looking twist. Conversations there focused on AI, automation, and the rise of vast biological datasets, and how they can reshape the industry into a tightly integrated “data, discovery, development” machine. The direction of travel is towards:

- AI-native discovery engines

- Automated, “lights out” labs

- New service models that treat biology as a data problem as much as a wet science problem

The result is a credible path to a multi-billion-dollar market in AI-enabled biotech services and platforms, and a broader sense that London sits near the centre of that emerging map. MedCity’s new “London Life Sciences Companies to Watch 2025” brochure, which spotlights more than 60 high-potential firms across biotech, medtech and health data, gives that optimism some tangible names and faces.

Industry gives its verdict on the budget

Behind the conference stages, the UK government announced further policies to grow science and innovation both pre-budget and as part of the budget. These can be broken into three main pillars:

The first pillar is UK Research and Innovation’s (UKRI) £38.6 billion settlement, which ministers are now carving more deliberately into distinct buckets.

Broadly:

- £9 billion is earmarked for critical technologies where the UK is already globally competitive, notably AI, engineering biology, cybersecurity, and quantum.

- £8 billion is assigned to mission-style priorities aligned with the Modern Industrial Strategy and national resilience, from clean energy and climate adaptation to flood defence.

- £7 billion is dedicated explicitly to innovative company growth, intended to unlock the next generation of scale-ups.

- £14 billion is reserved for curiosity-driven, investigator-led research, a nod to the reality that many breakthroughs cannot be planned.

Within that, engineering biology funding will almost triple to £644 million, and dedicated AI funding will more than double to £1.6 billion over the period. Early use of the £54 million Global Talent Fund is already luring world-class principal investigators to relocate to the UK, each bringing teams and projects in their wake. There is also investment into sustainable medicine manufacturing, as referenced in last week’s note.

The second pillar is the capital system that connects those labs to growth finance.

- The British Business Bank has published a new five-year strategic plan, backed by a £4 billion boost and a mandate to focus much more heavily on tech and life sciences scaleups rather than just start-ups and debt schemes.

- Over five years, its programmes are expected to support around 180,000 businesses, 370,000 jobs and add roughly £68 billion to GVA, with larger cheques into innovative firms that would otherwise struggle to find mid-stage capital domestically.

Alongside this, an initial £200 million fund is being assembled with three major pension funds (Aegon UK, NatWest Cushon and M&G). The aim is to prove that UK pensions can allocate meaningful capital into high-growth companies and to use the Bank as an origination engine for a much larger institutional flow over time.

In the background, the British Industrial Competitiveness Scheme, now out for consultation, would cut electricity prices by up to 25% for around 7,000 energy-hungry manufacturers in strategic sectors aligned to Invest 2035.

The third policy strand is sovereign AI capability. AI was mentioned 59 times in the Treasury’s official red book document.

- Ministers have announced an advance market commitment of up to £100 million under which the state acts as “first customer” for UK AI hardware start ups.

- A new AI growth zone in South Wales, taking the number of announced AI growth zones to four.

- A new Sovereign AI Unit, chaired by venture investor James Wise and backed by almost £500 million, is tasked with building out the domestic AI “stack”, from compute to hardware and software ecosystems.

- Up to £250 million of additional compute is being procured to support UK researchers and AI firms.

- Investment commitments from Grow, Graphcore, SoftBank, Cerebas, AI Pathfinder, Perplexity AI, Cursor, Microsoft, Vantage Data Centers and Equinix. While a lot of this is focused on infrastructure, there are also office openings and AI labs in Bristol, London, and Edinburgh.

- DSIT has published an AI for Science Strategy, backed by up to £137 million, focused on three pillars (data, compute, people, and culture) and five application domains: engineering biology, fusion, materials, medical research, and quantum technologies.

In practical terms, this means more GPU hours for labs, better AI-ready datasets from national facilities and a push to create autonomous lab platforms that can cycle experiments far faster than traditional setups.

The budget brought some additional announcements relevant for science and innovation:

- £300 million in tech for the NHS to improve patient services, potentially good news health tech and MedTech. This builds on the £10 billion allocated for digital spending as part of the 2025 spending review.

- The Enterprise Management Incentive (EMI) scheme is to be expanded to include more businesses from 6 April 2026.

- New London Stock Exchange listings will be exempt from Stamp Duty Reserve Tax (SDRT) for three years.

- Further devolution powers.

- The amount of money which can be raised by companies through EIS and VCT investments will increase from 6 April 2026.

- Corporation tax capped for the duration of parliament.

UK startups broadly welcomed these measures. Dom Hallas of the Startup Coalition commented: “In a tricky budget the chancellor made one thing clear – entrepreneurs and founders building high growth businesses are the engine of growth in the UK.”

The reaction was not uniformly positive, however. The budget quietly introduced an international student levy, setting off alarm bells in universities, who argued it sends a negative signal about the value placed on future innovators. Others stressed that substantially more capital will need to flow if the government’s ambitions are to be fully realised, and that ideas must be matched by execution.

On growth zones, critics noted that action must extend beyond place to tackling deeper structural issues such as energy constraints and talent shortages. Taken together, the budget and its pre-Budget announcements provide further evidence of intent but also underline how much more will be required to deliver on the promises made.

Europe’s academic startups come of age

Across Europe, university laboratories have become fertile ground for new businesses. Academic “spinouts” are now a cornerstone of the continent’s innovation economy. In the past decade, these ventures have proliferated and swelled in value. According to a recent report from Dealroom deep tech and life sciences spinouts from European institutions are collectively worth nearly $400 billion, having created some 160,000 jobs across over 7,300 startups. What’s more, the pace is quickening. Roughly 40% of that value was generated by spinouts launched since 2015, signalling an acceleration in value creation. Spinouts are also becoming a larger share of Europe’s new tech firms. Around 40% of all new deep tech and biotech startups since 2019, up 80% compared to 2010-2018 and 76 of Deep Tech and life sciences spinouts have reached $100 million plus revenues and/or $1 billion plus valuation.

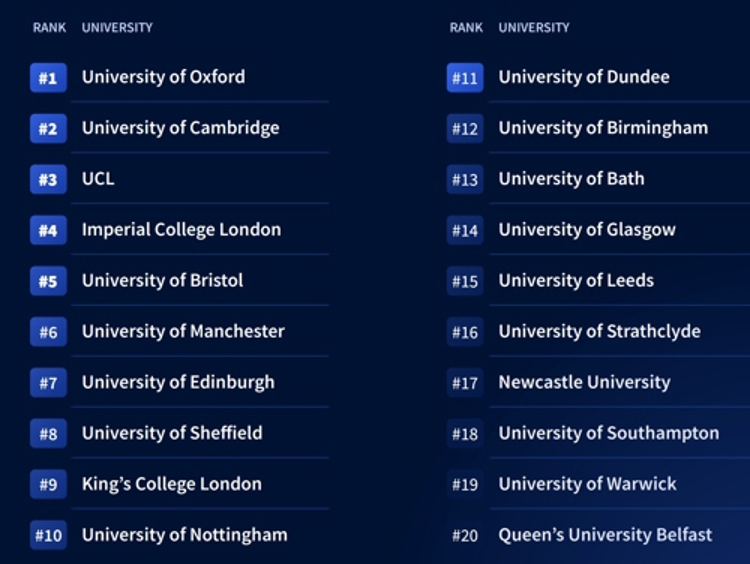

Within this European surge, the UK stands out. Home to two of the world’s most eminent research universities, the UK lays claim to Europe’s top two spinout engines Oxford and Cambridge and fully half of the continent’s ten highest-value spinout-producing universities (others in top ten are – UCL, Imperial College London and University of Bristol). Unsurprisingly, the UK leads Europe in the total enterprise value created by spinouts, outpacing larger economies like Germany and France. The UK’s 1,180-plus venture-backed spinouts have raised over $19.2 billion since 2020 and together are valued at around $114 billion. Oxford Science Enterprises is building a new company nearly every month, with a pipeline of over 125 companies attracting major investment and making real commercial progress. These figures underscore the UK’s strong science base and active investor community.

Yet the UK’s dominance comes with caveats. Several smaller countries outperform the UK when population is factored in. Moreover, success brings growing pains. The UK still wrestles with structural weaknesses that threaten to slow its spinout ecosystem. Industry observers note persistent gaps from fragmented university IP policies and capital constraints (including a heavy reliance on US investors for late-stage funding) to patchy infrastructure and a shortage of experienced scale up talent.

One striking trend is the changing geography of UK innovation. Spinout activity is spreading across the country. Of course, the Golden Triangle remains dominant but rising hubs such as Bristol, Nottingham, and cities in the so-called “Northern Arc” – Liverpool, Manchester, Leeds, and Sheffield now feature prominently on the UK’s spinout map. Edinburgh and Glasgow, too, are nurturing more spinouts.

The sectoral mix of spinouts underlines where the UK and Europe see their technological future. Life sciences and deep tech are twin pillars, each contributing roughly equal heft to spinout valuations and unicorn count. UK universities excel in biotech and medical research while also punching above their weight in computing and AI. Deep tech ventures, from quantum computing to novel materials, form a strong pipeline for the next generation of breakthroughs. Notably, quantum technology has made outsized waves despite a relatively small number of startups. The UK is at the forefront here, with ventures like Oxford Ionics and others leveraging university physics departments. Other specialised fields are also coming into their own. Academic spinouts dominate Europe’s nascent photonics and nuclear fusion sectors, and contribute significantly in areas like climate tech, semiconductors, and advanced manufacturing. By contrast, some industries such as conventional robotics, defence tech, even space launch see more activity from non-university startups.

Places that work: Lessons from the Netherlands

If Europe’s spinout numbers show what is being created, the Knight Frank VITALS Innovation Study Tour to the Netherlands offers a glimpse of where these companies want to live. Across five days and eight Dutch cities, the Australian and UK delegation saw an ecosystem that treats innovation not as a stand-alone “park” but as a core organising principle of urban development.

Key lessons include:

Triple and Quadruple Helix Governance: Structured collaboration is not just rhetoric-it’s systematically embedded in governance, funding, and tenancy. Government, academia, industry, vocational education, and community partners co-create the rules and culture of innovation precincts.

Vocational and Applied Pathways: Hogescholen and applied sciences institutions– equivalent of Australian TAFEs – are deeply integrated in every Dutch precinct, producing not only pathway graduates but the technical, operator, and mid-tier talent essential for innovation ecosystems. Vocational training is a core strategic partner, not an adjunct.

Critical Mass and Clustering: Regional clusters like Medical Delta demonstrate how deliberate density and co-location drive resilience, collaboration, and scale. The Brainport regional cluster alone contributes ~3% of Dutch GDP, showing that scale is engineered - not accidental.

One Health and Convergence: Integration of human, animal, plant, and environmental sciences—with digital and AI as fundamental cross-cutting capabilities – accelerates translational research and global differentiation.

Applied Research Backbones: Netherlands Organisation for Applied Scientific Research (TNO) plays a central role: embedded, connected nationally, and relentlessly focused on industry translation, adoption, and scale-up across all clusters.

Sovereign Capability: Successful Dutch precincts are not just real estate, they anchor national security in semiconductors, biotech, and vaccine production.

Data as Infrastructure: AI, digital platforms, and open data are treated as sovereign, not optional, assets. Data is embedded in every aspect of ecosystem design, underpinning research, mobility, housing, and collaboration.

Open Innovation and Transparency: Collaboration, IP sharing, and data openness are built directly into operations, tenancy, and governance. Ecosystem curation is active and visible, not simply assumed. Investment horizons are measured in decades, not years.

Storytelling Anchors Value: Dutch precincts use clear narratives, metrics, and proof points to demonstrate global relevance and attract partners.

Other interesting reads

Underscoring that we are in a global race for dominance in innovation, the US launched its “Genesis” mission for AI, which Trump likened to the Manhattan Project. Actions include expanding computational resources, increase access to vast federal datasets and move toward impactful, real-world applications, particularly in scientific fields.

HP announced a restructuring plan that will involve 4,000 to 6,000 layoffs, as it aims for savings of about $1 billion by fiscal 2028. A number of tech giants, including Amazon and Microsoft, have also undertaken layoffs in recent months, while ramping up their AI efforts.

Procure Ai, a London, UK-based company that provides AI-native procurement automation solutions, has raised $13 million in Seed funding.

London VC Firgun Ventures has unveiled the first $70million (£53.4million) close of its quantum-focused investment fund.

Further orders for UK defence secured at the Dubai airshow. The government also reconfirmed plan to further invest in defence.

Sign up to Knight Frank Research.