Strong Start to H2-2025 for the UK Hotel Sector

A robust Q3 has allowed UK hotel operators to reverse much of the first-half declines, following an upbeat period of trading in Q3, with all key performance indicators (revenues and profitability) turning positive year-on-year.

Stronger forward bookings translated into robust Q3 RevPAR growth, of 4% in London and 4.1% in regional UK. Consequently, as at September YTD, London’s RevPAR is almost level with 2024, and across regional UK, 1.5% ahead.

London

London’s upper-mid and upscale hotels achieved the strongest occupancy growth of 3.6 percentage points in Q3 to reach over 90% occupancy, and whilst y-o-y ADR growth was constrained to half a percent, this segment recorded the highest RevPAR growth of all segments, a rise of 4.8%. Meanwhile, London’s luxury hotels achieved the weakest ADR growth of all London segments in Q3, just marginally ahead of 2024, but enjoyed a respectable y-o-y rise in Q3 occupancy of 2.5 percentage points.

As at September YTD, an average uplift in London’s TRevPAR (total revenue per available room) of 0.5% was recorded, restoring the 1.9% y-o-y shortfall suffered in H1-2025. However, TRevPAR for London’s upper-upscale hotels, which began Q3 with the largest deficit, remained some -2.5% below Sept-YTD 2024 performance.

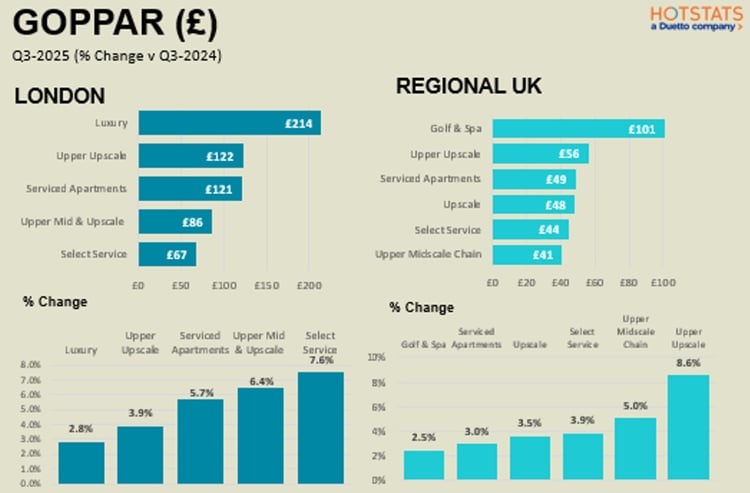

Meanwhile, the y-o-y shortfall in London’s GOPPAR as at Sept-YTD has reduced to -3.4%, compared to -8.9% for H1-2025. A reduction in YTD-2025 utility costs of 6.6% PAR has supported GOPPAR and profit margins.

In Q3, the most robust GOPPAR performance came from select-service hotels, and upper-mid and upscale hotels, with an uplift of 7.6% and 6.4%, respectively. In doing so, the YTD annual GOPPAR shortfall remained at -1.9% for both segments.

Regional UK

Regional UK’s upper-upscale hotels recorded the highest Q3 growth in RevPAR of 5.3%, and with equally robust growth from F&B and Leisure revenues, maintained y-o-y TRevPAR growth at the same level. Meanwhile, for Golf & Spa hotel which saw the strongest growth coming from ancillary revenues, achieved an uplift in Q3 TRevPAR of 4.2% annual growth.

As at September-YTD, regional UK is now tracking ahead of 2024 in terms of TRevPAR by 1.6%, with Golf & Spa hotels outperforming the regional market, with YTD TRevPAR growth y-o-y of 4.7%.

Meanwhile, the H1-2025 shortfall (-5% versus H1-2024) in Regional UK’s GOPPAR has almost been restored following the robust Q3 performance, with September YTD GOPPAR of £37.70 just 0.6% below the profits achieved over the same period in 2024. Golf & Spa hotels was the only segment to record GOPPAR growth, ahead by 1.1% over the same period. Upper-upscale hotels achieved the strongest Q3-GOPPAR growth, which has allowed YTD GOPPAR to be back on par with the previous year.

Profit margins across all regional hotels also improved, with a marginal uplift to 37% in Q3. Yet, only minimal cost savings were made from utility costs across regional UK, which declined by less than 1.0% PAR, as Q3 recorded utility costs rising by 3.1% PAR.

Sign up to Knight Frank Research