Ski Resorts, Super-Prime and Shifting Taxes

Plus, the Alpine pivot to year-round markets and Italy’s new flat-tax era

Plus, the Alpine pivot to year-round markets and Italy’s new flat-tax era

As Europe heads into a pivotal 2026, the property landscape is shifting fast — from Alpine resorts reinventing themselves as year-round investment hubs to Italy recalibrating its tax regime and major markets across the continent regaining momentum. Below is a snapshot of the key forces shaping where capital is flowing, how wealth is moving, and what to watch next.

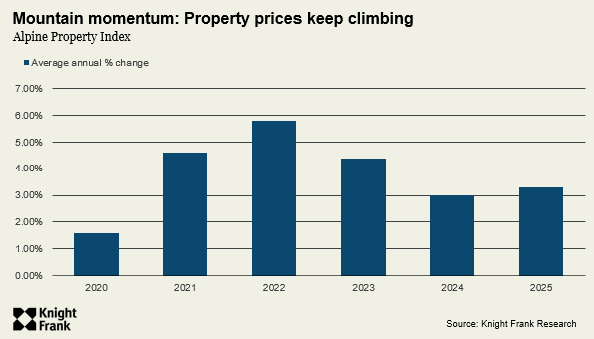

Knight Frank’s latest Alpine Property Report finds the mountains are still outpacing global prime real estate, with prices up 23% in five years as Europe’s leading resorts pivot from seasonal ski escapes to full-fledged, year-round investment plays.

Standout performers:

Demand shift: A structural pivot is under way: 73% of HNWIs, rising to 80% of millennials, would consider full-time Alpine living. Summer lift-pass sales in Chamonix jumped 46% since 2021, underscoring year-round appeal.

Climate resilience: The Alpine Sustainability Index ranks Val Thorens, Val d’Isère and Zermatt highest for long-term snow reliability, while lower-altitude resorts diversify into cycling, hiking, culture and wellness.

Download the full 32-page Alpine Property Report here for the complete picture.

Italy’s tax landscape is about to shift. From 1 January 2026, Rome will overhaul elements of the Flat Tax regime — a change with clear implications for internationally mobile UHNWIs and long-term relocators.

What’s changing?

From 2026 onwards, newcomers will face a higher rate.

Current beneficiaries retain their existing rate.

The reforms aim to curb “tax tourism”, increase revenue, whilst still remaining competitive with regimes in Portugal, Greece and Switzerland. At the same time, proposals to raise income-tax thresholds for mid-earners may offer some support to broader housing demand.

Italy is also tightening its holiday rental rules and regulations. Expect more uniform registration standards, city-level consistency and potential caps in high-volume markets such as Florence and Venice.

These efforts could temper speculative buying while improving long-term rental availability - a growing priority for policymakers under pressure to address affordability.

Market signals

So what? Italy is signalling fiscal discipline — but not a retreat from attracting international capital. Prime markets including Rome, Milan, Tuscany and Lake Como remain underpinned by global liquidity and continued supply shortages.

Europe will enter 2026 with cautious optimism. Eight ECB rate cuts have revived sentiment, liquidity is returning, and prime residential markets are leading the recovery.

Market momentum:

Investor confidence is rebuilding as lower borrowing costs and infrastructure investment help sustain housing demand.

Wealth inflows:

Regulation reshaping value:

Bottom line: Europe’s residential recovery is uneven but strengthening. Lower rates, structural demand and record wealth inflows support a positive 2026 outlook. But risks remain: weaker trade, political uncertainty in key 2026 elections, rising public debt (on track for 130% of GDP without reform) and the IMF’s 0.5% downgrade to Europe’s growth outlook could limit momentum.

Read the full European Outlook 2026 for the complete analysis.

Swiss Set to Reject Inheritance Tax on Super Rich, Poll Shows (Bloomberg), Bulgaria to join Eurozone in 2026 (FT), ECB to stay on hold before year-end (Bloomberg) and French Government touts investment as tax concerns mount (Bloomberg).

Sign up to Knight Frank Research.

Sorry!

An unexpected error has occurred.

Please try again later.