UK Student Market Update Q3 2025

Investors commit more than £3.4 billion to the PBSA market so far this year, even amid a more challenging letting environment for the 2025/26 academic year.

Investors commit more than £3.4 billion to the PBSA market so far this year, even amid a more challenging letting environment for the 2025/26 academic year.

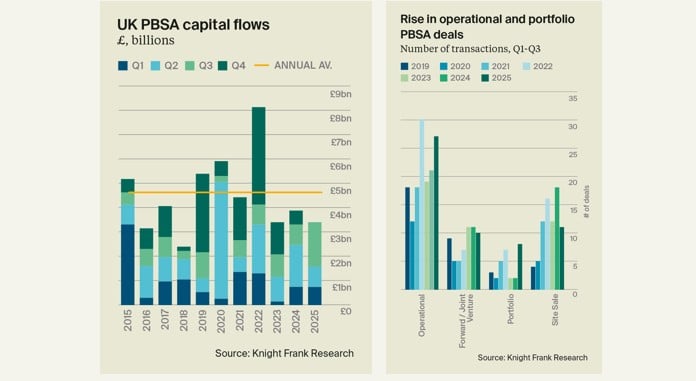

July to September marked the largest third quarter on record for UK PBSA investment volumes, with £1.83 billion passing hands. This takes investment volumes in the year to date to circa £3.4 billion, up 3% on the comparable period in 2024. A number of key deals transacted over the course of the quarter including QuadReal’s acquisition of the Apollo Portfolio for more than £550 million, and KKR’s purchase of the Curlew Capital Portfolio for a price in the region of £230 million.

Whilst the numbers suggest a liquid investment market, capital markets intelligence suggests deal times have been prolonged in some cases. Investors have a clear appetite for first generation standing stock assets – where there is upside potential to deliver value-add returns. But for these deal types, fire safety, remediation work, and a later leasing cycle is contributing to elongated transaction timelines.

While single asset operational stock still accounts for the largest share of investor activity, with 27 assets sold so far this year, there has been a resurgence in portfolio transactions in 2025. In total, nine portfolios have traded over the year-to-date. A preference for portfolios reflects investor appetite for scale across core-plus and value-add platforms, even amid a more challenging letting environment for the 2025/26 academic year.

Relative to recent peaks, land sales (11 transactions) and forward funding opportunities (10 transactions) have slowed in the nine months to September. Significant delays at the Building Safety Regulator as a result of Gateway 2, planning challenges, and high build cost environment have all had an impact on capital allocation on land and funding pathways to the UK PBSA market. A lack of clarity on timing of Gateway 3 at the end of construction presents further challenges to viability.

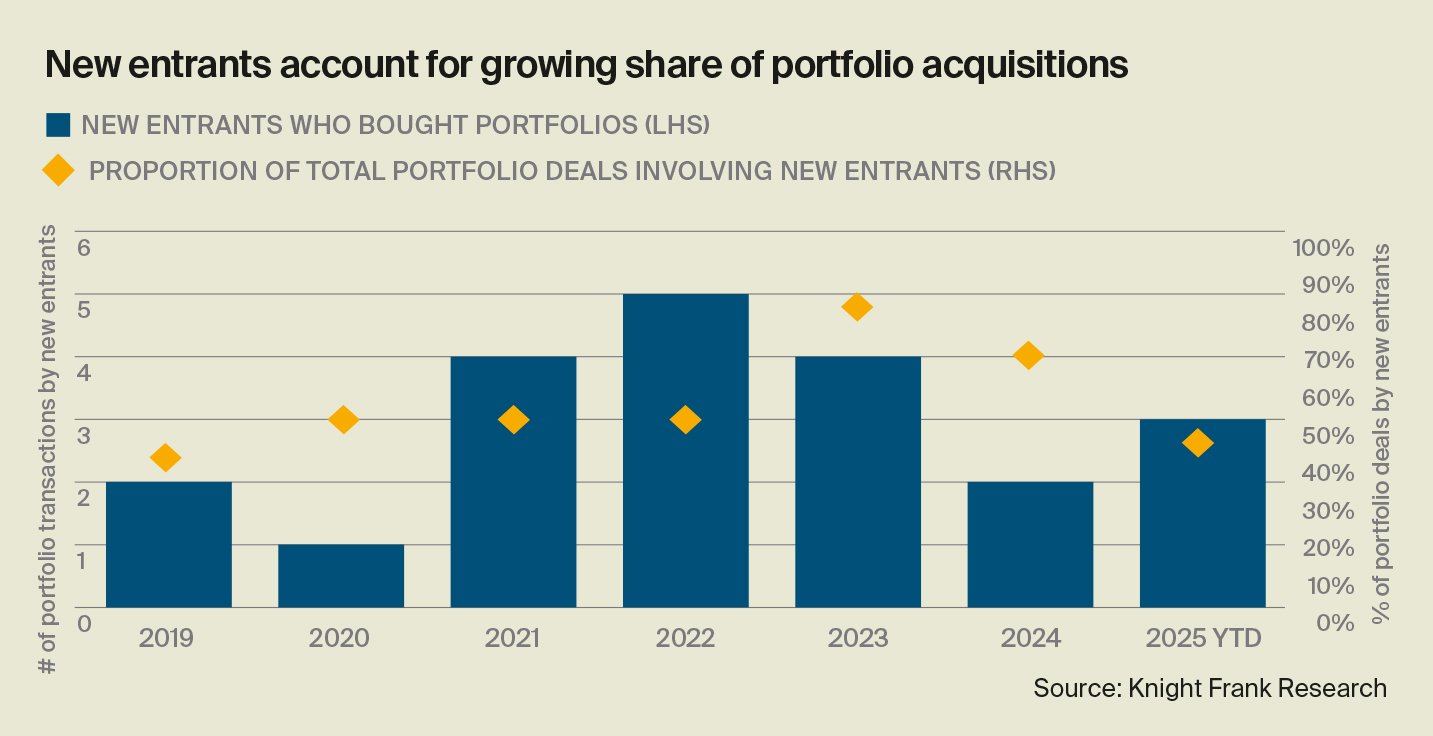

A rise in new entrants and the return of existing players showcase the attractiveness of the UK PBSA sector for global capital allocation. Our analysis reveals that, since 2019, new entrants have taken a growing share of portfolio transactions. New capital sources accounted for 67% of total portfolio transactions last year, and so far in 2025 have accounted for 44% of portfolio sales. This momentum is expected to continue.

Established players remain the core component of the UK PBSA investment market, but with new capital sources looking for best in class assets and/or first-generation assets with potential to deliver value-add returns, the liquidity pool has deepened.

As expected, the Bank of England (BoE) kept interest rates at 4.00% during its September monetary policy committee meeting and announced the decision to dial back its quantitative tightening bond-selling programme from £100 billion to £70 billion. The quantitative tightening target is in line with the BoE’s wider monetary policy plan to effectively reduce the banks’ balance sheet, while ensuring not to impact the government’s wider gilt issuance strategy. Andrew Bailey, Governor of the BoE, suggested the UK economy was ‘not out of the woods yet’, and while inflation stayed flat in August, unfavourable base rate effects will likely mean inflation will rise in the September reading, and any further rate cuts will need to be made gradually and slowly.

Despite an optimistic view amongst some forecasters that BoE base rate could fall up to 100bps to 3.00% by the end of 2026, lingering fiscal concerns and softer economic outlook suggests property yields will stay elevated relative to 10-year government gilts, at least in the medium term. However, the UK is not alone in this scenario, with the spread between long-term government bond yields and property yields a global phenomenon for investors.

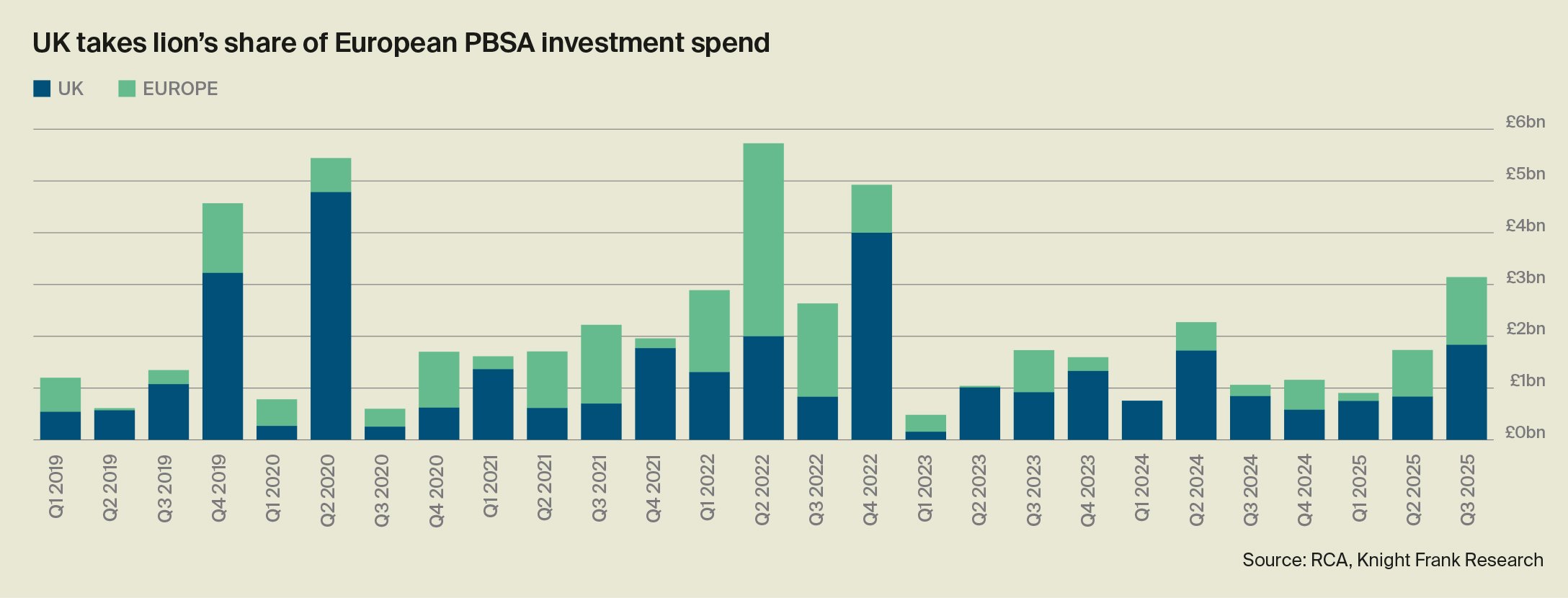

But investors can see the wood for the trees. For real estate, stable income growth rather than yield spreads, is what will drive capital growth returns in this cycle. For PBSA investors, fuelling the income return story is focusing on markets with favourable demand-supply imbalances, and assets with expected value appreciation. Despite a more favourable debt landscape in Europe of late, UK assets have captured the lion’s share of capital spend in PBSA across the continent, accounting for approximately 60% a quarter since 2019.

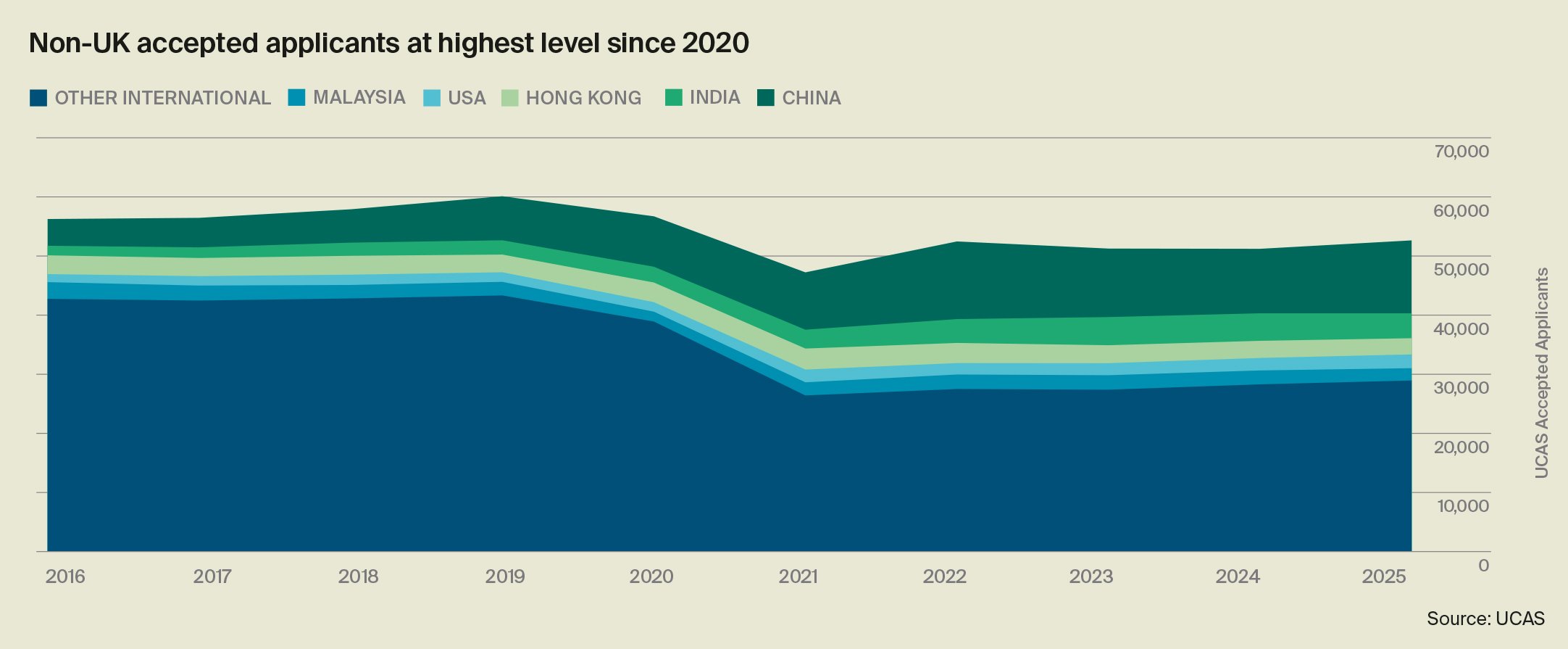

UCAS results day data points to a strong undergraduate admissions cycle (2025/26), particularly for higher-tariff institutions. Overall acceptances are up 3.1% year-on-year, with UK acceptances rising 3.2% and international acceptances increasing 2.8% to their highest level since 2020. Notably, Chinese acceptances have rebounded by 13.1% to 12,380, and US acceptances are up 10.4%, although India and Malaysia saw modest declines.

Higher-tariff universities continue to strengthen their position, accounting for 39% of all acceptances (up 6.9% year-on-year) and 69.4% of international students – the highest share since 2016. Meanwhile, 82% of applicants received their first-choice university, with 18-year-old UK entry rates up to 32%.

Despite robust results on acceptances from UCAS, a cautionary upbeat tone should be taken when interpreting the data for the overall Higher Education Sector. UCAS is representative of the future of undergraduate students only and is not indicative of postgraduate enrolments.

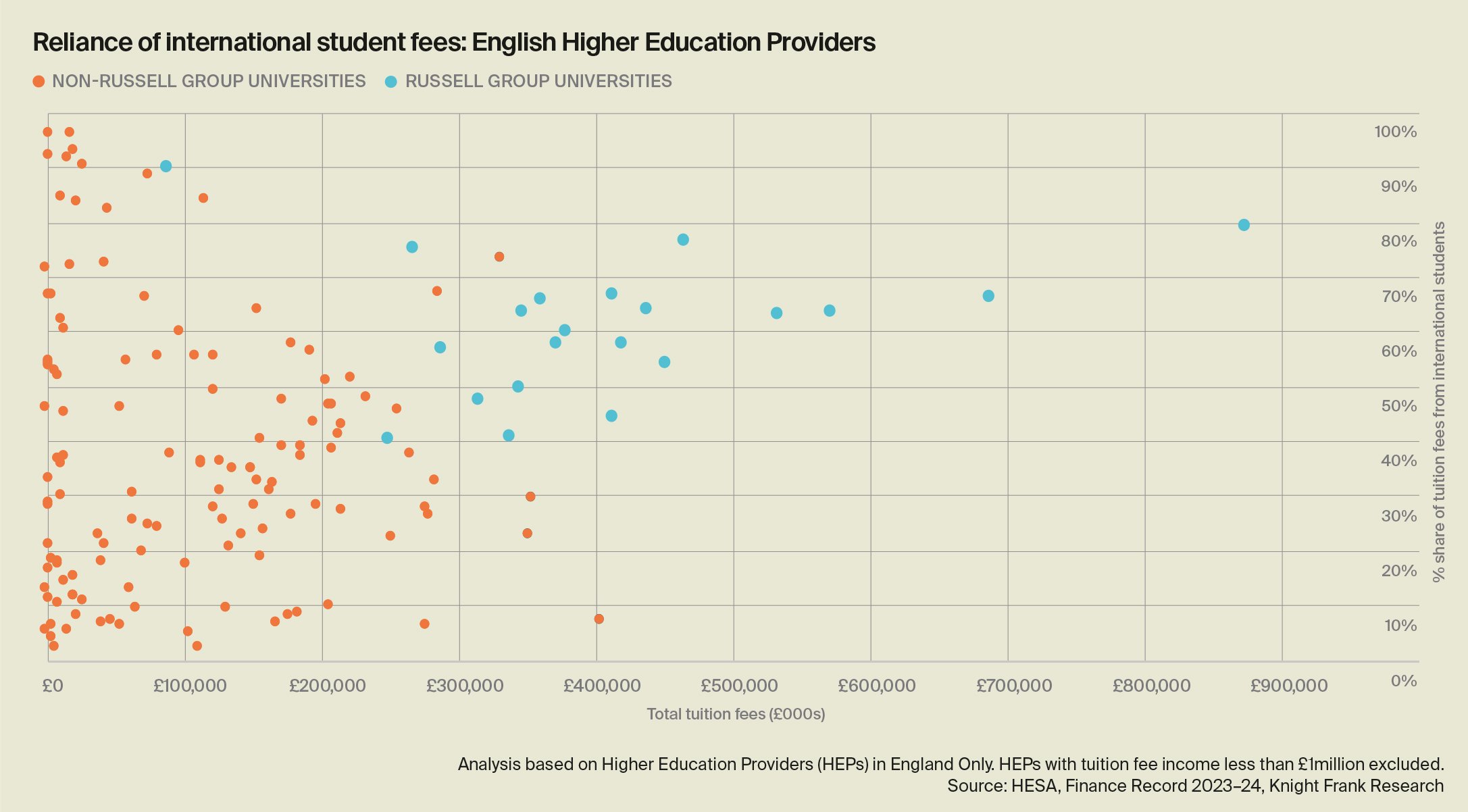

The UK government has confirmed that an international student levy will be introduced in England, despite opposition from the higher education sector. While details are yet to be finalised, the levy is expected to be around 6% of universities’ income from international students. Revenue raised will fund the reintroduction of means-tested maintenance grants for domestic students on priority courses aligned with government missions and the industrial strategy under the Lifelong Learning Entitlement. Further information is expected in the Autumn Budget on 26th November. The levy is likely to increase fees for international students as universities seek to recover costs, potentially impacting the UK’s competitiveness in the global education market. Early indications suggest that higher-tariff institutions may weather this more easily, leaving mid- and lower-tariff universities most exposed to financial strain.

The big questions deserve a deeper dive – and they’re coming in our UK Student Accommodation Outlook 2025/26, launching this November. We’re covering everything from our latest PBSA rental growth results, occupancy trends, and where the next investment opportunities lie. In addition, it will also cover the results from our sixth Knight Frank/UCAS Student Accommodation Survey. Sign up to our newsletter to stay informed.

Sign up to Knight Frank Research.

Sorry!

An unexpected error has occurred.

Please try again later.