UK Property Market Outlook: Week Beginning 8 February

Average rental values in prime central London are the lowest they have been in a decade. It is drawing people back to central areas in a sign that the “escape to the country” story has a shelf life.

3 minutes to read

While property market headlines have been dominated by the “rural exodus” happening in the sales market during the pandemic, a shift in the other direction has been taking place in the lettings market.

Last month we showed how more people are moving to Canary Wharf due to cheaper rents and the ability to walk to work. The same effect has been seen more widely across central London as people take advantage of the benefits of living in zone 1.

It underlines the strength of demand for urban living when the price is right, suggesting there are natural economic limits to the “escape to the country” story. As we highlighted in November, asking prices for large central London flats had fallen by more than any other property type, which may tempt investors able to see through the short-term fog of Covid-19.

“There has always been a group of people living on the periphery of central London who couldn’t afford to go in any further,” said David Mumby, head of Prime Central London lettings at Knight Frank. “That has changed and we’re seeing movement from areas including Wandsworth and as far away as Croydon into Chelsea and South Kensington.

“This fundamental reset of rental values means there has almost never been a more affordable time to rent in central London,” said David. “The allure of PCL hasn’t gone away and tenants are thinking beyond lockdown. People working from home like the idea of being close to central London amenities and parks. They are taking advantage while this window of opportunity stays open. Once international travel resumes it will start to close.”

Average rents fell by 13% in prime central London in the year to January, which took them back to levels last seen at the end of 2009 during the global financial crisis.

There are two primary reasons for this, both of which are temporary. First, a glut of short-let properties has appeared on the long-let market due to successive lockdowns. Second, demand from overseas students and corporate tenants has fallen away.

As a result, more tenants from outside zone 1 are able to move to central locations.

The number of new prospective tenants registering in prime central London who came from outside the area was 35% between June and December 2020, up from 26% in the same period in 2019. Furthermore, their average distance from the boundary of PCL more than doubled to 3.1 miles from 1.5 miles over the same period.

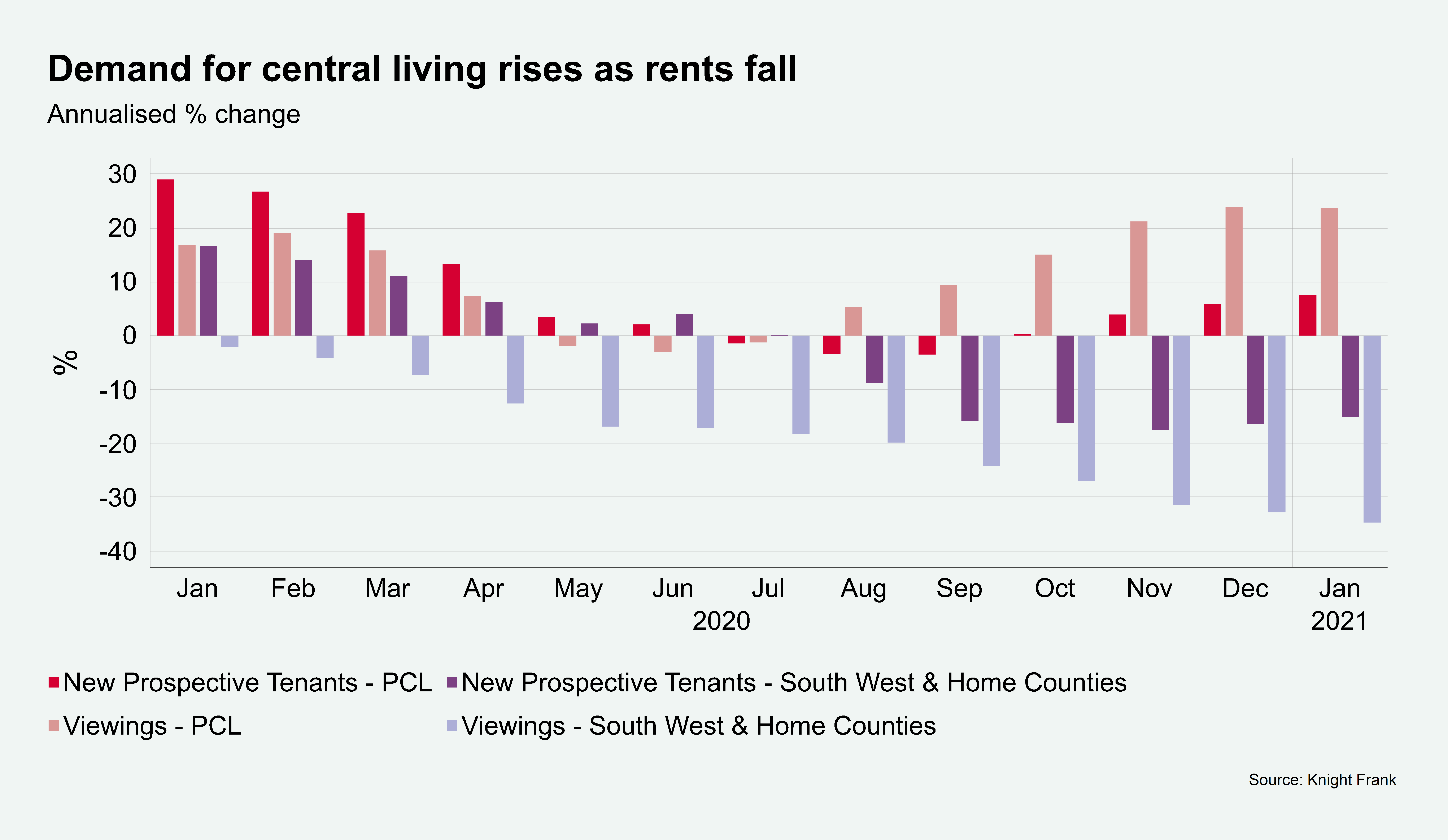

In a mirror image of what has happened in the sales market, falling rents have driven demand for central London when compared against south-west London and the Home Counties, as the above chart shows. Areas including Wimbledon and Richmond have seen more modest single-digit rent declines as the stronger sales market has meant less supply transferring to the lettings market.

While the number of viewings in PCL rose 24% in the year to January 2021 versus the previous 12 months, there was a 35% decline in south-west London and the Home Counties. New tenant registrations were up 8% in the same period in PCL while the number declined 15% in south-west London.