Covid-19 in Africa: Focus on North Africa

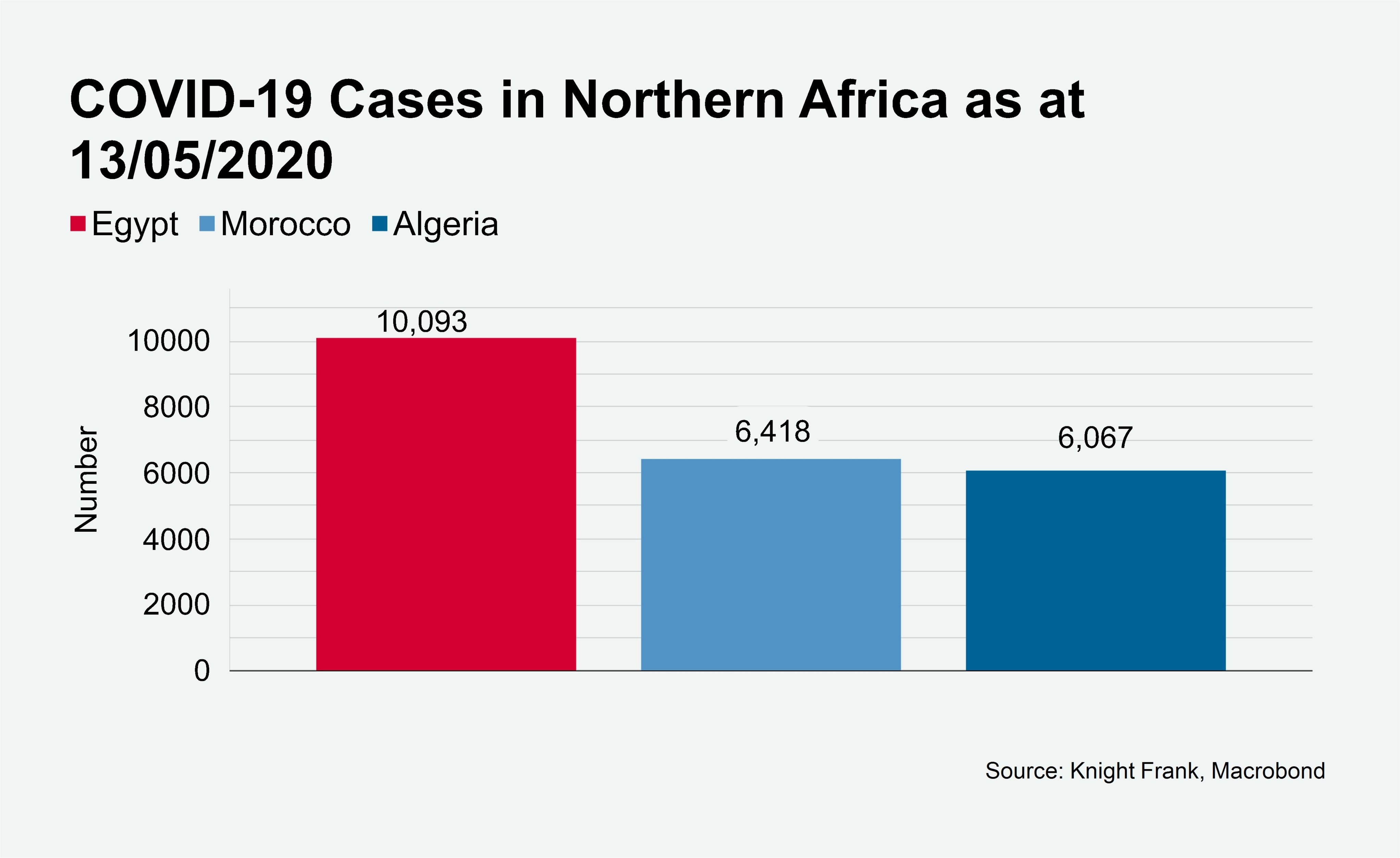

Within Africa, North African countries have recorded the highest numbers of Covid-19 cases. While economic outlook in the region has previously been clouded by political uncertainty, the impact of Covid-19 on individual economies is expected to vary depending on which sectors are prevalent in each economy.

28 February 2021

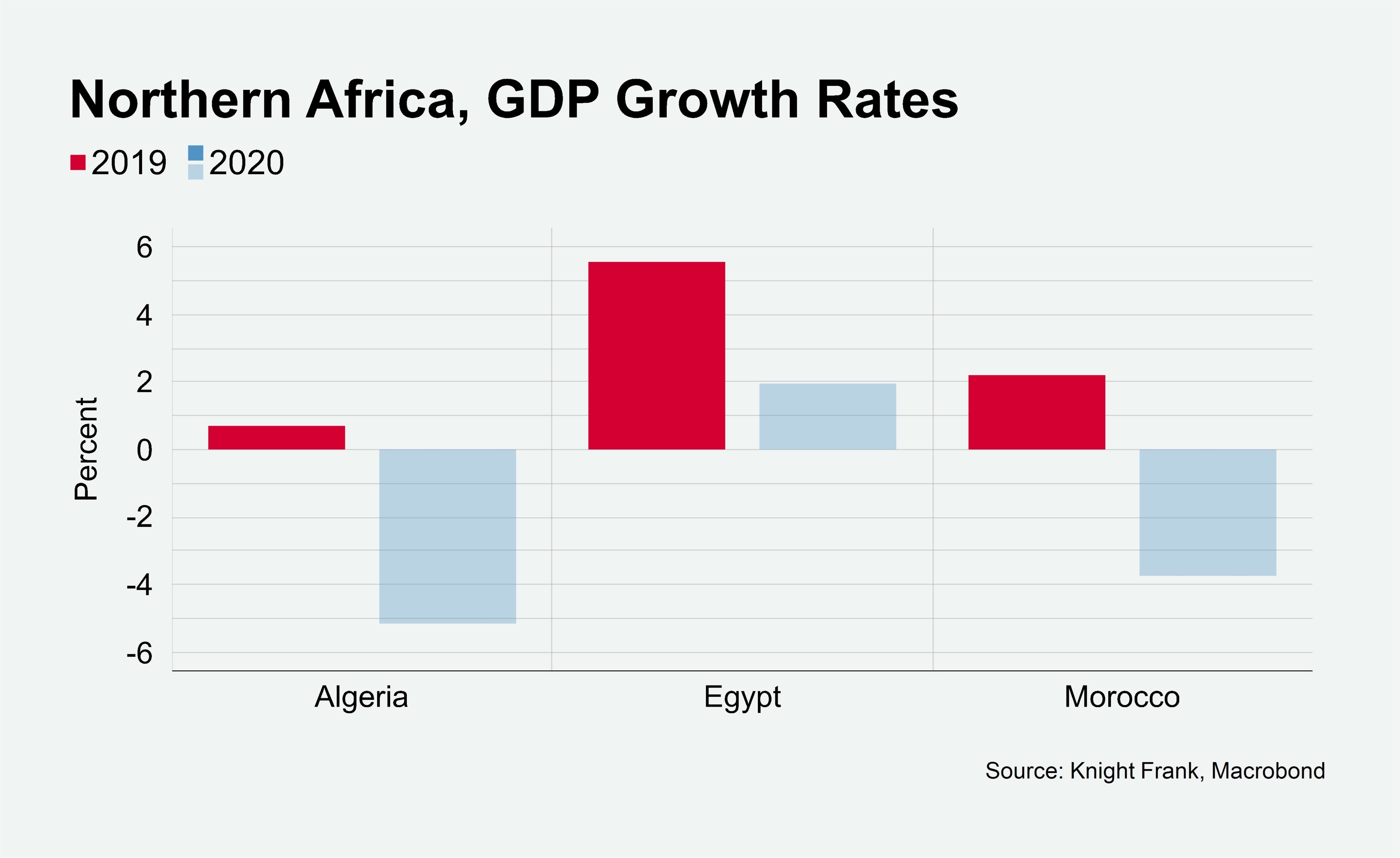

In Algeria, the pandemic’s impact has been exacerbated by plummeting oil prices and continued political uncertainty. The IMF has projected that the country’s GDP will contract by 5.2% in 2020 down from 0.7% growth rate witnessed in 2019 before rebounding t oa 6.2% growth rate in 2021.

In Egypt, the pandemic is anticipated to disrupt the recent steady economic growth, which has been attributed to the 2016 IMF’s macroeconomic stabilisation program. The pandemic’s impact on the country’s tourism sector and export revenues is set to significantly increase Egypt’s financing needs, with the IMF already providing US$2.8 billion in additional funding. Despite these challenges, according to the IMF, Egypt’s economy is expected to remain the most resilient in the region with GDP growth projected at 2.0% in 2020, down from 5.6% in 2019.

Disruption in the tourism and manufacturing sectors due to the pandemic coupled with the current impact of drought on the dominant agricultural sector, are anticipated to push Morocco’s economy into a recession for the first time in more than two decades. The IMF has projected that Morocco’s economy will contract by 3.7% in 2020, down from the 2.2% growth rate in 2019, before rebounding to a 4.8% growth rate in 2021.However,as a net oil importer, the rapid fall in oil prices and access to funding are likely to ease the pressure on the country’s economy.

|

Algeria Fiscal & Monetary Policies

Government Interventions

|

|

Egypt Fiscal & Monetary Policies

Government Interventions

|

|

Morocco Fiscal & Monetary Policies

Government Interventions

|

Source: IMF Policy Tracker

Impact on Real Estate Sectors

Further to the above government interventions, we analysed market activity in the different real estate sectors, across the region between March and April 2020. While the level of impact has varied across different sectors, the retail and industrial sectors have been severely impacted as a result of the pandemic across the region.

In Morocco, residential transactions have been halted as a result of the closure of notary offices due to the imposition of lockdown measures. Rents in the sector are expected to record slight declines of not more than 20% with the possibility of recovery by the end of the year. In the commercial sector, occupiers are looking to renegotiate their leases in order to obtain greater levels of flexibility. Rent defaults have primarily been recorded by small and medium occupiers, where these missed payments have been classified as debt rather than default as a result of government interventions. Furthermore, state-owned offshoring parks have offered the possibility of delaying payments or making monthly payments. We expect rents will decline slightly by not more than 10% due to the limited supply in prime offices.

Algeria’s relative independence from foreign markets has been a safety net in terms of the initial impact on the real estate market. In the commercial sector, all active transactions have been delayed including the shift of most banking institutions and multinationals to the Bab Ezzouar financial district. In the residential sector, developers have started to incentivise sales rather than leases in a bid to absorb any potential future impact from the crisis.

In Cairo, rents across the commercial and residential sectors have remained stable. However, commercial and residential developments have stalled as a result of the containment measures adopted by the government.