The Global Healthcare Note - October 2020

Six months into the pandemic: views from our global healthcare and senior living team

7 minutes to read

Knight Frank’s global healthcare and senior living team, spanning five continents, annually advises on £150bn plus of assets, has collaborated to provide a succinct update of the COVID-19 pandemic in respective markets.

Global summary

News feeds around the world reported that the global death toll for COVID-19 reached 1 million, in late September. This was of course a bitter pill to swallow, especially when you consider that the real figure is probably much higher, and that some nations have been tackling the outbreak for as long as ten months with severe economic and social implications. Spread across 188 countries, recorded cases are now above 37 million (Worldometer), although this is in part due to increasing levels of testing.

Many European countries are in the onset of a second wave of the virus, after the relaxing of social restrictions revealed that COVID-19 is no less infectious. Furthermore, while efforts to develop a vaccine are underway, the minimum time frame for trial and distribution is at least two years (and typically much longer) – Even the most optimistic of us concede that we will still be dealing with virus well into 2021 and there will be some significant legacy effects. So the key question is not how long the pandemic will last, but how effectively we can contain it and treat it.

Will the global economy take precedence? Government’s round the world remain in the spotlight with the huge task of balancing further social restrictions against the threat of economic damage. They must also contemplate the mental health burden and social inequalities that may arise from further lock downs. These will be very tough decisions, especially in colder climates where the winter brings greater dependence on indoor activity and usual winter illness such as seasonal flu tend to peak.

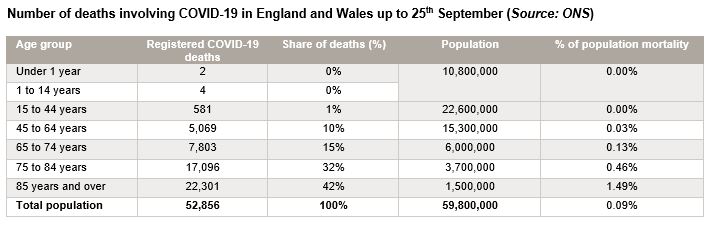

How is residential care shaping up? One thing we do know is that global elderly populations need protection and health and social care needs to be high up the political agenda. Retrospective data in the UK confirms that close to three quarters of fatalities have occurred in those over the age of 75 – a population group that drives demand for care beds and senior living residences. However, the same data also shows that mortality rates (number of COVID-19 deaths divided by population) have been low, despite the level of health vulnerability in the elderly population. This confirms what we know from direct conversations with many of our elderly care and senior housing operators across the regions – the sector has scrambled incredibly well to protect residents thus far and is even better prepared to control the virus in the winter ahead.

Insights from across our global network

Europe & UK

In the UK, much of the narrative is currently focused on the rise of the so called “R number” and the threat of a winter wave of the virus. While care home operators have endured circa 30,000 excess deaths thus far, the mortality rate within the sector peaked as early as April and normalised to pre-pandemic levels as early as June. Knight Frank independent analysis also shows that occupancy declined by a moderate 8% in the second quarter and has since stabilised with operators beginning to confidently admit new residents again. From an infection control perspective, operators are now in a much stronger position with rigid procedures in place to protect residents and staff.

The UK seniors housing market has also shown resilience in the face of COVID-19. We are seeing increasing institutional investment into the sector, with investors attracted to stable inflation-linked long-term income and diversification into ‘beds’ from more established asset classes.

Both Spain and France have seen considerable increases in cases and infection rates in recent weeks, and EU health officials have subsequently called member nations into more action to avoid another disabling lock down. According to the ECDC’s 14-day cumulative tracking, Spain has in excess of 300 cases per 100,000, France has 248 and the UK follows slightly behind the curve with 190 (as of October 7th). Germany continues to be viewed as the benchmark among developed economies. As of the end of September, the country had experienced circa 10,000 deaths and over 307,000 cases in a population of 84 million (Worldometer). A number of measures have been attributed to these low numbers, including: early establishment and high levels of testing, successful protocol for containing the virus among the elderly, and ample hospital capacity.

North America

The 2020 election is dominating news feeds in the United States, and the government’s handling of the pandemic will be a feature of the debates. The US has seen over 215,000 deaths, but as with the election, the story varies hugely across regions and states. The East coast, including NYC, is particularly wary of a second spike as people begin to move indoors as the climate changes. The West coast has seen cases decline markedly and investor sentiment towards the healthcare sector is increasingly positive, especially with the accelerated emergence of telemedicine as key branch of the tech sector. Canada has also seen the emergence of a second wave of the virus in recent weeks, but is in the process of implementing a multi-layered testing strategy.

North American healthcare property investors have resigned to the view that the next 18 months will be restrictive, but are generally bullish on healthcare. Analysts expect to see an increasingly active market, with operators tightening belts and looking to raise capital via sale leaseback of real estate assets. With a backlog of opportunities and development projects in the pipeline, 2021 is predicted to be busy for the seniors market.

APAC & Middle East

Rather than a swift and deadly spike in the virus in the Spring, India saw an initial steady rise in cases across the summer months, before a more rapid rise from August onward. India now has well circa 7 million recorded cases across its population of 1.4 billion (Worldometer), which has been enough to put its underdeveloped hospital system under pressure. Despite this, the virus mortality rate in India is seemingly low, and instead the economic impact has been high up the agenda. Following lock down, GDP contracted 24% year-on-year in the second quarter and growth is at only 3%, prompting concerns that the governments’ long-term healthcare investment strategy may be hampered. Property investors are currently focused on India’s emerging office and logistics sectors, the latter of which has been the biggest gainer in pandemic.

The UAE, an emerging hub for medical tourism, is now welcoming medical tourists back from elsewhere in the Middle East and the globe. After an early and swift lock down helped to limit the virus, emirates like Dubai are reopening their medical services and pressing on with strategies to be global medical and wellness destinations with big implications for real estate markets. There is no shortage of appetite and capital for the healthcare sector in the Middle East, and this is epitomised by Saudi Arabia’s AMAALA gigaproject which seeks to build a giant wellness tourist destination on the Red Sea.

Australia & New Zealand

The Australian Government have extended a temporary job keep support scheme to support businesses and their employees until the end of March 2021. That said the level of subsidy provided is being reduced – a decision that has received mixed reviews as the country faces its first recession in nearly three decades. Mirroring the United States, the infection rate remains hugely varied across regions of Australia and this is reflected in the restrictions imposed by various states. Restrictions have been especially draconian in Melbourne, hampering constructions, the property valuation inspections required by bank lenders, and therefore the wider commercial property market. The spate of imported cases seen in New Zealand in August served to justify strict measures seen across the continent.

Should you have any further questions please contact Julian Evans- Head of Healthcare.

For specific research queries, please contact Joe Brame from our commercial research team.