Prime London Sales Report: September 2020

Prime central London sales index 5299.5

Prime outer London sales index 255.7

1 minute to read

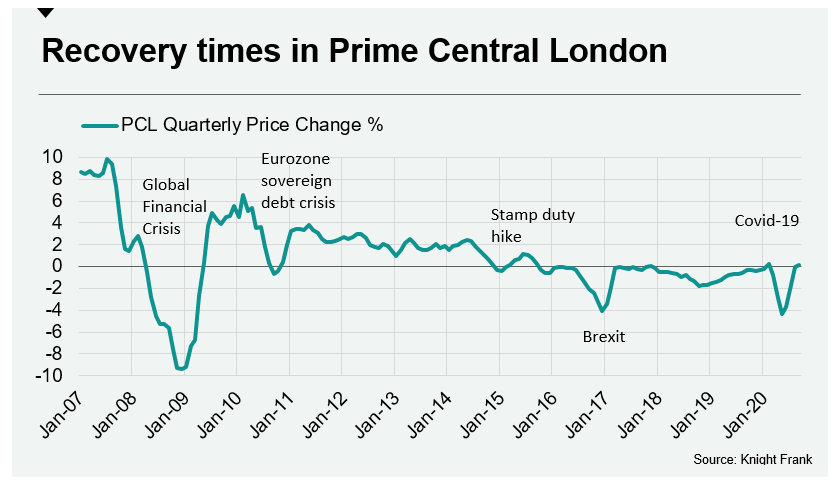

Quarterly price growth returned to the prime central London property market in September for the first time since February this year.

An average increase of 0.2% was the same figure recorded during the so-called ‘Boris bounce’ that followed the general election in December 2019.

While ‘bounce’ is not the best description for what happened in prime London markets between July and September, there was a notable recovery from the period of marked uncertainty that caused prices to fall in Q2.

This recovery followed six consecutive months of quarterly price falls in PCL, which is shorter than the 13-month run of declines during the global financial crisis, as the chart below shows.

In prime outer London, September marked the second consecutive month of rising prices over a three-month period. It meant the annual price decline narrowed to 3.9%. This stronger performance has been driven by an increase in demand for family houses and more outdoor space since the lockdown.

In a year when demand has ebbed and flowed so dramatically, the recovery is still fragile.

Demand remains strong compared to previous years but there are signs it won’t be as resurgent during Q4 as it was in Q3.

The number of new prospective buyers registering in London was 44% above the five-year average in the week ending 3 October. That increase has halved since July and August. We have also reported on how the number of price reductions across the country has edged up in recent weeks.

However, while the initial post-lockdown surge in activity has subsided slightly, it is important to acknowledge that transaction activity will remain strong in Q4 due to the length of time it will take for deals agreed in the summer to reach completion, as we explore in more detail here.