University acceptances up and student accommodation bookings in line with expectations

New survey data on bookings for purpose-built student accommodation (PBSA) points to strong leasing activity.

3 minutes to read

One of the big question marks for universities and student accommodation providers over the last few months has surrounded what will happen to domestic and international student numbers for the coming year. Both have been grappling with trying to understand the potential impact a significant drop in undergraduates could have on future income when the new academic year starts in September.

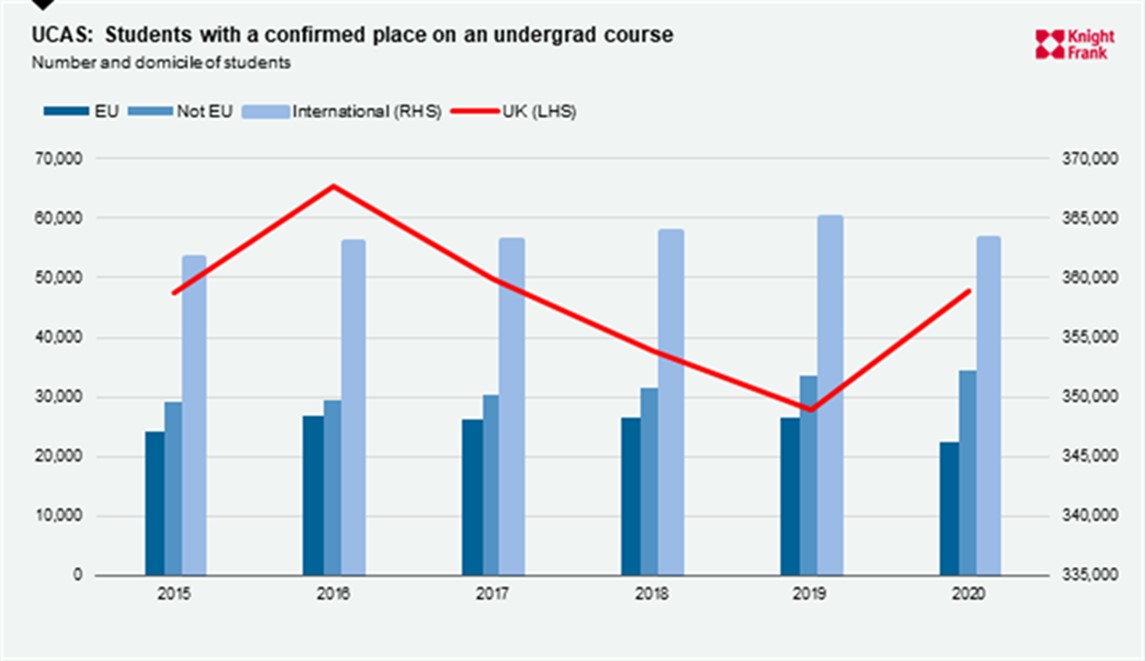

A-level results day has provided us with a much clearer picture as to where we stand. And the initial figures paint a fairly positive picture. Admissions body UCAS says a total of 415,600 students have a confirmed place on an undergraduate course in the UK, which represents a 1.6% increase compared with the same point last year.

Across the UK, 30.2% of all UK domiciled 18 year olds have been accepted through UCAS – a record high proportion for results day. The equivalent figure for 2019 was 28.2%.

Crucially, just 4% (14,370) of placed UK students are currently planning to defer starting their course, which is the same proportion as at this point last year, and suggests that the Covid-19 pandemic - and subsequent changes to course teaching patterns - hasn’t materially changed students desire to go to university this year.

But what of international students? The UCAS data suggests that 34,310 students from outside the EU have been accepted into UK universities, up 2% on the same time last year. However, acceptances from students within the EU have fallen by 15.2%, to 22,430.

This means that overall the number of international students with a confirmed undergraduate place at a UK university is down 5.5% on the equivalent point in 2019. However, there are currently more international applicants holding an offer, and their places will be confirmed once their qualification results are provided to universities.

So, student numbers – particularly domestic ones - look to be holding up with no red flags at this stage of the process, but how does this translate to the student accommodation market?

Knight Frank recently completed a snapshot survey of six of the largest UK student accommodation operators who between them control 170,000 beds in the sector, equivalent to 25% of the total number of student beds in the UK.

Currently, based on this survey, bookings are between 70% and 85% of what was expected for this cycle overall. The average across the operators surveyed is 77% of beds booked for this coming cycle.

The picture across different markets will vary significantly based on the balance between the demand and supply of accommodation. Operators across all markets will be gearing up for what is likely to be a more important clearing period this year with the expectation that more students will be placed at university through this process. Markets containing universities that are more reliant on the clearing process to fill courses may well have a very late end to the booking cycle as a result.

The results of the poll demonstrate students’ ongoing commitment to going to university this year. PBSA operators have seen higher levels of demand than first anticipated, and are going into the ‘clearing’ process with a robust average occupancy rate.

Considering the ongoing market headwinds, underpinned by the strict social distancing measures and restrictions on international travel, it is reassuring to see that PBSA is weathering the storm well.

Photo by Helena Lopes on Unsplash