Steppin’ Out into London’s Walkable Business Districts

People are excited about the 15-minute city. The idea has generated a huge amount of buzz across property and politics amid a wider rethink of how we build and manage cities in the wake of the pandemic. There’s a lot to like. Building communities in which everything you need, from groceries, to leisure to work, are within just 15-minute walk would generate huge benefits to health and wellbeing and it also taps into changing buyer, tenant and occupier requirements post pandemic. But how do London’s CBDs stack up on this measure, and what is the opportunity for real estate?

3 minutes to read

Changing requirements

It’s clear that what we want from the built environment has changed. One aspect of that is a greater appreciation of our surroundings.

In the housing market, among other factors, that means wanting amenities on our doorstep. In fact, when asked ‘What is important when choosing somewhere to live?’ nearly two thirds of the London respondents to our latest client survey said being close to local amenities is more important now than pre-pandemic. Some 34% said the same about being within walking distance to work.

It’s a trend equally relevant to office occupiers looking to draw on the deepest pools of talent. Some 46% of occupiers surveyed in our latest (Y)our Space report said they expect a greater amenity offer from their workplace in the next three years.

For real estate investors it adds weight to the arguments for building mixed-use, mixed-income, walkable places, or at least benchmarking schemes or sub-markets against their closeness to commercial, retail, transport, leisure and health facilities.

Defining walkability

The Knight Frank Walkability Index has been developed to provide insight into the current built environment. Applying it to seven central London sub-markets, it analysed more than 140,000 Ordnance Survey Addressbase points, identifying 9,000 amenities of interest for walkability. These were then grouped into six sub-categories; Arts, Culture and Tourism, Education, Food & Beverage, Green Spaces and other Health & Wellbeing, Retail and proximity to Transport nodes, generating an overall walkability score based on count.

How do London’s CBDs score?

In isolation, London’s existing sub-markets score well for walkability. Overall, the West End Core tops our analysis, followed by the City Core, Southbank and Canary Wharf. However, often these high scores are underpinned by a dominance of a single sub-category. Further analysis of the West End Core, for example, shows that retail accounts for 70% of its total walkability score.

In comparison, other sub-markets, such as the Southbank, boast a more balanced mix. Perhaps unsurprisingly, these are also the markets which have a higher number of homes. It is interesting to note that the top two, and more mature submarkets, for residential population have also seen office rental growth twice the average of the market overall. Moreover, both submarkets maintain below average levels of availability, have seen substantial gains in property values and show greater resilience in economic downturns.

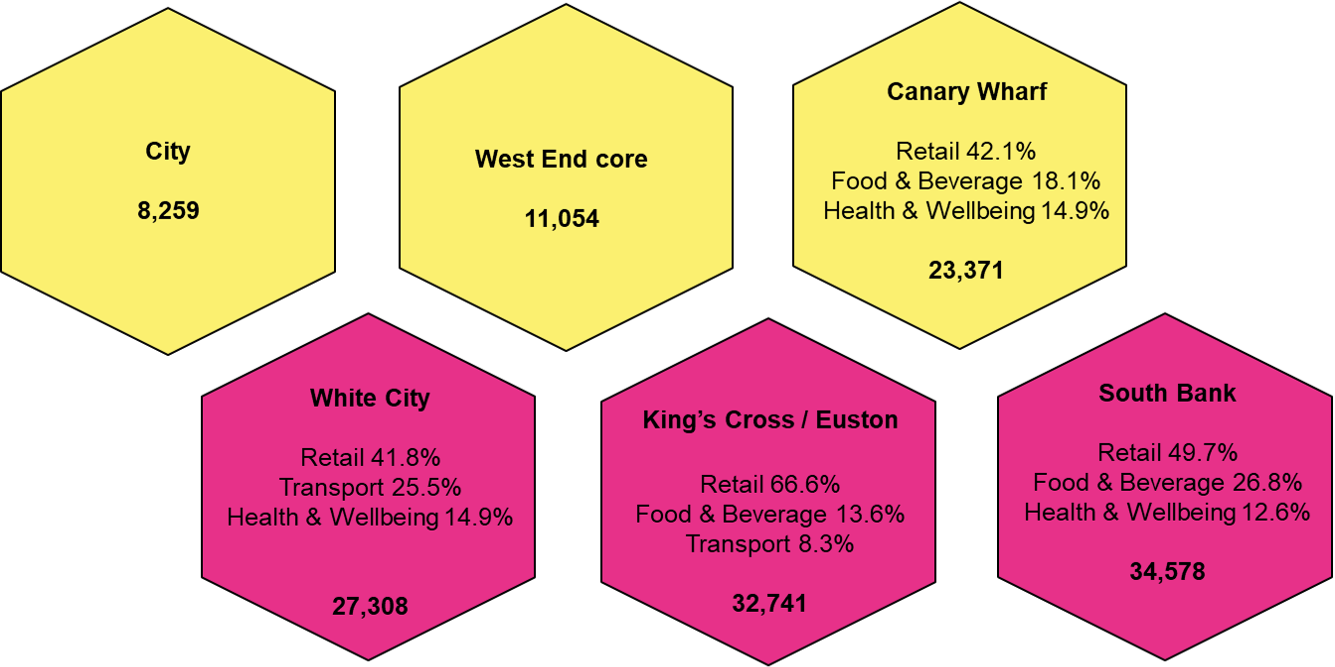

Figure 1: More residents in Southbank within 15 mins walkability of amenities.

Top three contributors to walkability score, No. of people within 15 mins walkability of amenity offer

Source: Knight Frank Research

We explore the potential opportunity for repurposing assets elsewhere in the London Report but, clearly, changing working, shopping and living habits point to a need for more balanced mix in the future. It is a fact also recognised by city planners. Last year, the City of London Corporation, announced plans to create at least 1,500 new homes by 2030 by repurposing offices and other buildings left empty because of the pandemic.

Balanced and sustainable

The next opportunities will lie in schemes and in areas that start or continue to evolve into a balanced, resilient, and sustainable mix of real estate - think about what’s been delivered at King’s Cross, Battersea, the Southbank, or what’s coming at Brent Cross, Canada Water, Earls Court or Euston. Equally, there is an opportunity for existing amenity rich core locations, like those analysed above, to deliver refurbishments or through the repurposing of assets.

Meeting ESG goals

There are wider societal and environmental benefits which can stem from creating walkable neighbourhoods, a fact which is likely to be particularly relevant as the UK looks to set out a route map towards becoming a fully decarbonised nation, and developers and investors look to hit ambitious targets.

Walkable places which promote healthy, sociable and active lifestyles will be a key component.

Watch the virtual London Breakfast on demand.

Download the London Report 2022