Daily Economics Dashboard - 13 April 2021

An overview of key economic and financial metrics.

2 minutes to read

Download an overview of key economic and financial metrics on 13 April 2021.

Equities: Globally, stocks are mostly higher. In Europe, gains have been recorded by the DAX (+0.4%), STOXX 600, CAC 40 (both +0.3%) and the FTSE 250 (+0.2%). In Asia, the KOSPI (+1.1%), TOPIX (+0.2%) and Hang Seng (+0.1%) were all higher on close, meanwhile the CSI 300 closed -0.2% down and the S&P / ASX 200 closed flat. In the US, futures for the S&P 500 and Dow Jones Industrial Average (DJIA) are both +0.1%.

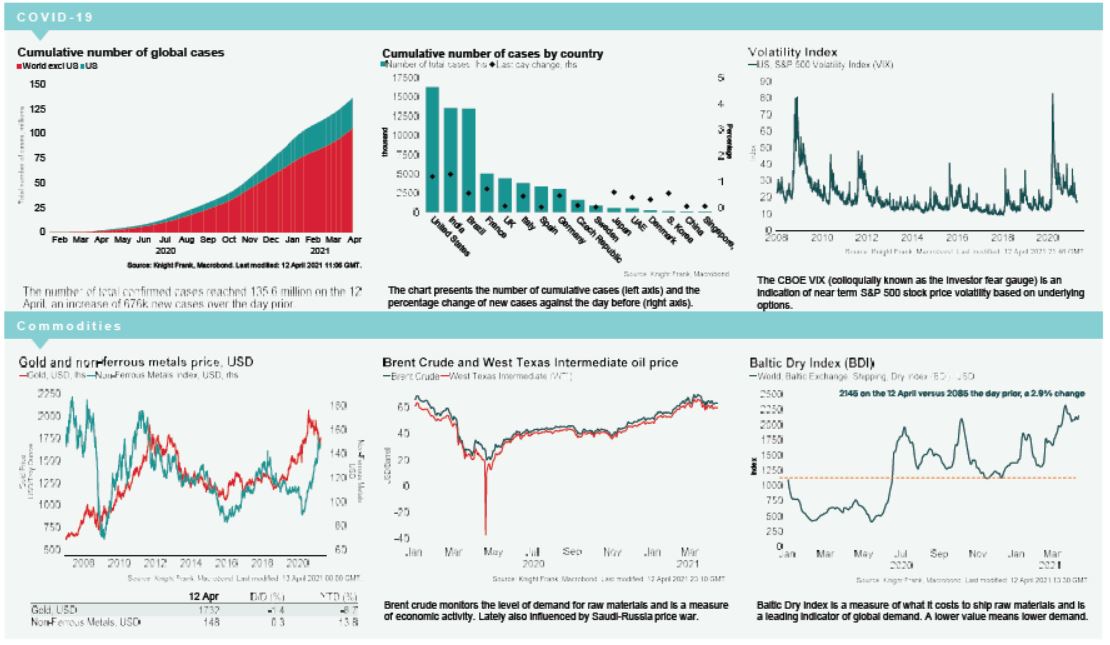

VIX: After increasing +1% over Monday, the CBOE market volatility index has decreased this morning, down -0.4% to 16.9, remaining below its long term average of 19.9. The Euro Stoxx 50 volatility index is also lower, down -4.2% to 16.3, remaining comfortably below its long term average of 23.9.

Bonds: The US 10-year treasury yield has softened +2bps to 1.69%, while the UK 10-year gilt yield and German 10-year bund yield are both up +1bp to 0.80% and -0.29%, respectively. The US treasury yield and German bund yield are both currently at their highest level since the end of March.

Currency: Sterling has appreciated to $1.38 and the euro is currently $1.19. Currency hedging benefits for US dollar denominated investors into the UK and Eurozone are at 0.60% and 1.78% on a five year basis.

Oil: The West Texas Intermediate (WTI) has increased back above $60 per barrel for the first time since the end of March, after increasing +0.5% this morning to $60.15. Brent Crude is also higher, up +1.0% to $63.88, its strongest level in nearly two weeks.

Baltic Dry: The Baltic Dry increased for the first time in three sessions on Monday, up +2.9% to 2,145, its highest level in two weeks and its largest daily increase in nearly a month. Prices were pushed upwards by capesize rates which increased +8.6% yesterday to a three month peak. The index is currently +57% above where it was at the start of the year, albeit -8% below the March peak of 2,319.

Chinese Exports: China’s exports in US$ terms increased +30.6% over the year to March 2021, following a +60.6% annual increase over January and February combined. This saw exports grow +49% y-y in Q1 2021, up from +16.7% in Q4 2020. Oxford Economics expect momentum to remain robust in Q2, however global shipping delays could undermine the near-term export outlook.