Hotel Dashboard - Covid-19 UK Hotel Market Recovery October 2020

Localised lockdowns bring continued uncertainty for the UK hospitality sector, but the situation remains highly fluid. We bring you our latest analysis of HotStats market intelligence, to chart, monitor and forecast the UK Hotel sector’s recovery.

3 minutes to read

In this first edition of the Hotel Dashboard, we provide our own opinions and outlook for the UK Hotel sector, together with a more detailed review of regional UK trading performance. Specifically, we compare the performance of two datasets of hotel located in regional UK - Select Service Hotels and Full Service, Upper Upscale hotels.

Download the Knight Frank Hotel Dashboard.

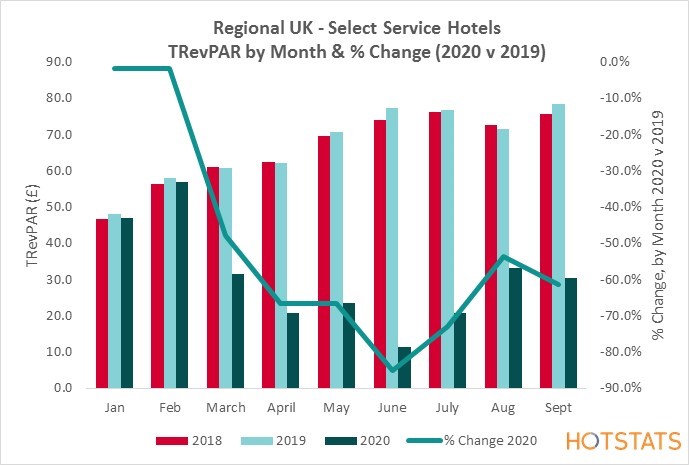

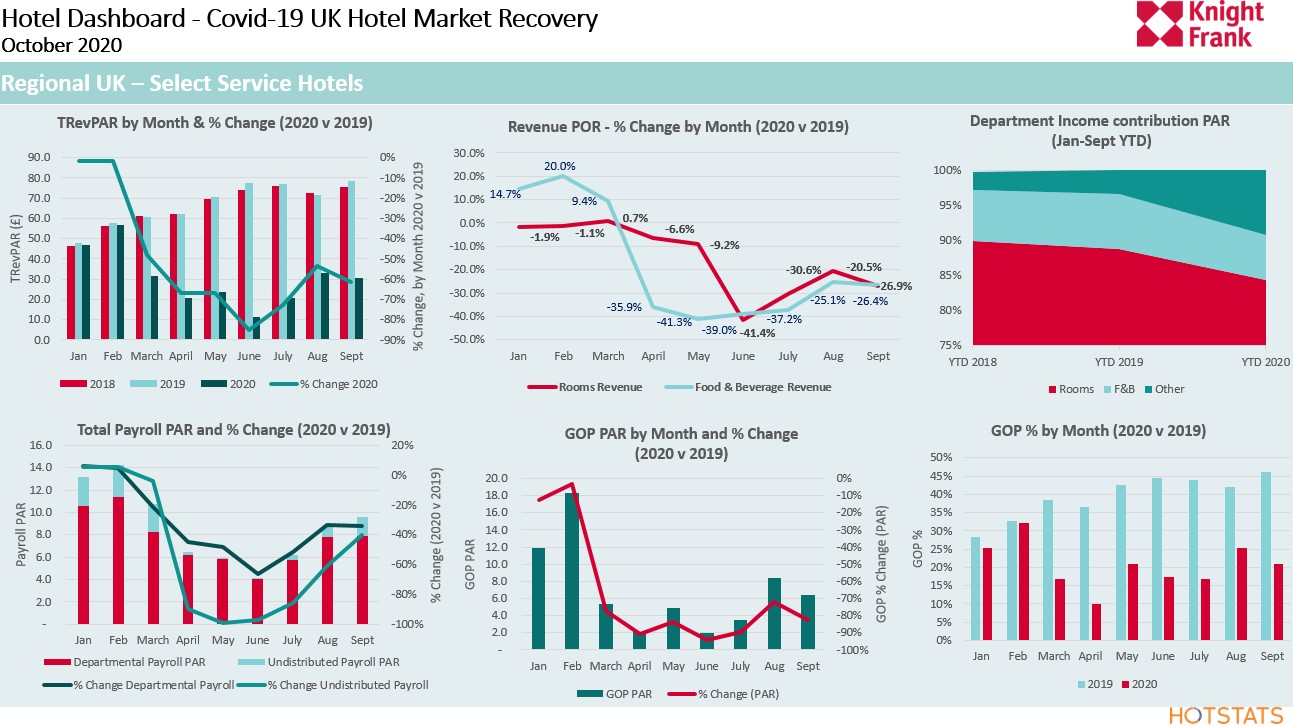

- Despite the extreme challenges presented by the pandemic, certain sub-sectors have proven their resilience. Select Service and midscale hotels in regional UK have experienced a less severe decline in TRevPAR compared to full-service, Upscale and Upper Upscale properties.

- The UK Staycation market is set to remain robust in 2021, due to ongoing global spread of the virus. Restrictions in cross border / international travel continue; and only limited forward planning is possible due to the situation constantly evolving.

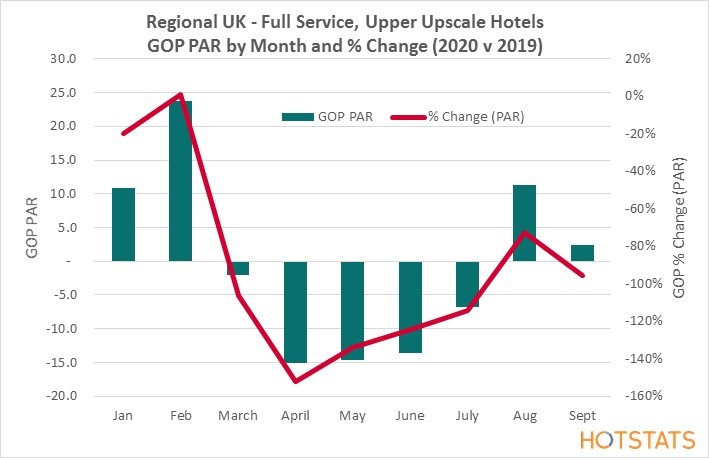

- The staycation boom during the month of August resulted in positive GOPPAR for the first time since the end of the lockdown across all Regional UK datasets; but with little or no growth in TRevPAR throughout September, combined with additional payroll costs, GOPPAR growth has been restricted across much of the regional UK hotel market.

- The Serviced Apartment sub-sector continues to outperform all of our hotel datasets under review, achieving 34.0% GOP as a percentage of turnover. With the sector benefitting from a versatile, flexible and lean business model, and, a physical product that provides space, privacy and independent living.

- UK short-stay, leisure demand is expected to drive recovery of the UK hotel market, where restrictions permit, with improving demand possible over the winter period, for UK towns and cities as leisure destinations. The price point and value proposition of the budget and select service hotels is expected to drive recovery in occupancy, as both corporate and leisure guests watch their spending during these uncertain times.

“Whilst the COVID-19 pandemic is having an unprecedented impact on the UK hotel market, it is also accelerating the growth in demand for both experience-led hospitality and the health and wellness sector.

“We also envisage there will be some structural changes in demand during the recovery period. Changes in the office sector are already starting to generate additional demand for hotel meeting space, with further growth likely as companies downsize or even do away with their office space over the coming years. With remote working set to continue post the pandemic, larger cities are expected to benefit from a rise in short-stay corporate and meeting demand, as people who have relocated return for face-to-face meetings.”

“In the absence of a global vaccine, with new tiered restrictions in place across the country and whilst overseas travel to the UK also remains heavily restricted, the focus in the short-term remains one of survival. Learning to constantly adapt to the changing landscape is critical.”

Karen Callahan, Knight Frank, Head of Hotel Valuations

Knight Frank Contacts: