Farewell to Furlough – what comes next?

With furloughing schemes starting to unwind and with growing concerns over what this will mean for employment, consumers and property markets we take a closer look at the latest data.

3 minutes to read

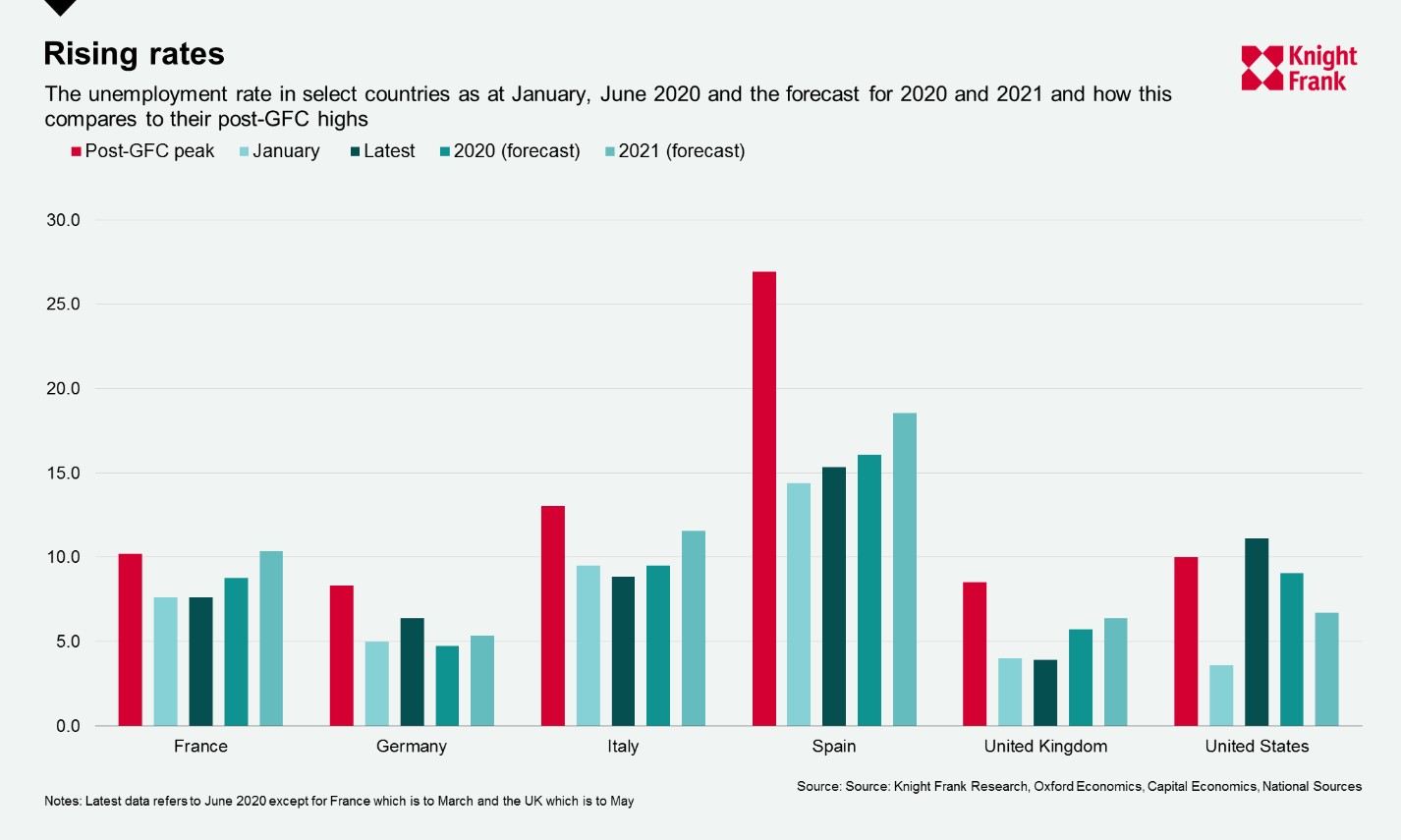

Whilst unemployment rates have risen only modestly in many key markets, the unwinding of job support schemes could signal a bleaker outlook over the coming months. However, many governments have committed to do whatever it takes to protect jobs, and constant review of these schemes provides some room for optimism.

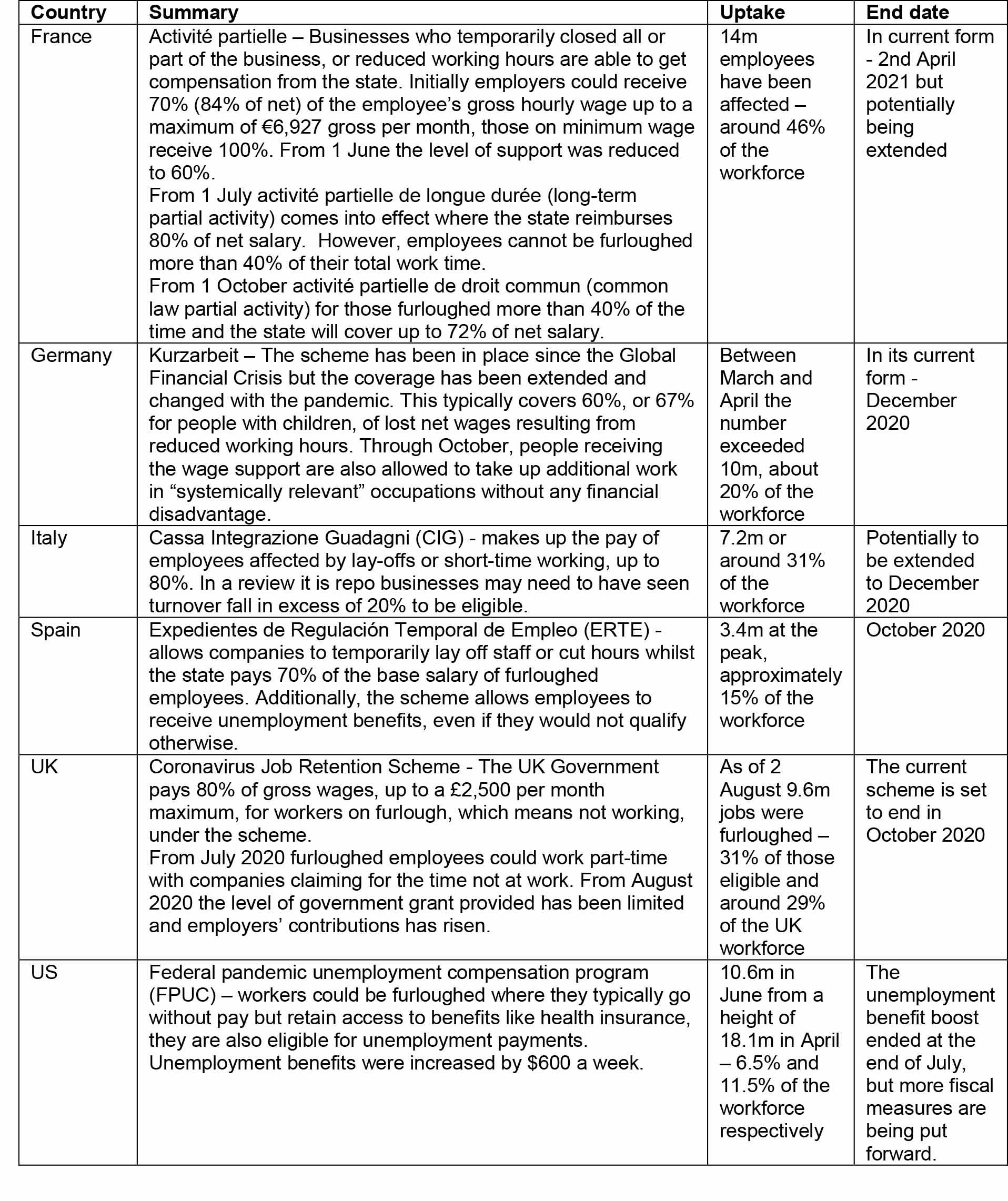

As demonstrated in the table below, many schemes in their current formats are beginning to wind down. As the threat of a resurgence in cases and disrupted economic activity continues governments may look for more options to support for a longer period.

Unemployment and housing

As unemployment rises, homeowners and tenants will find it harder to meet housing costs. This week Deloitte’s analysis of the US Census Bureau’s weekly household pulse survey, found that 87% of borrowers managed to meet the previous month’s payment, 7% failed, and 5% had payments deferred. This translates to roughly 5.5% of the adult population either leaving mortgages unpaid or deferring in May. On a positive note, given the scale of disruption, this is a marginal increase on the 4% in October 2019 and provides a degree of optimism.

With the level of unemployment benefits unwinding there is cause for concern. Deloitte’s analysis show that the most recent data indicated that almost 20% of adults in owner-occupied housing units used stimulus payments or unemployment insurance to meet spending needs in the last seven days.

As the US Government weighs a new round of stimulus it will be important to see how these impact on the unemployed, temporarily or not. Given the level of take-up of furloughing schemes and government support in other markets – see table below – the ongoing support could be vital for markets.

The level of job losses in the US has been watched globally and the figures include those temporarily out of work. Over 54 million new jobless claims have been filed since mid-March. However, this only paints half the picture.

In April the unemployment level reached 20.6 million, with over three-quarters, 78% of these, being temporarily unemployed. In June, the unemployment level fell to 14.3 million with 60% of these temporarily so. The US unemployment rate has been falling as activity resumes, despite rising case numbers, and is expected to fall according to forecasts (see figure below).

The UK Government is also looking to unwind its furloughing scheme in October and there have been many job losses already announced with this likely to continue. According to a survey of more than 500 companies by the British Chambers of Commerce, conducted in late July, 32% are expecting to cut jobs in the next three months. Despite the bonus for retaining employees only 43% of businesses would seek to use this and far fewer stated they intended to use the other schemes.

Silver lining – whatever it takes should support

Even as the current schemes, and their scheduled closures stand, the rate of unemployment in many key markets is still set to remain far below the levels seen in the wake of the GFC and Eurozone crisis.

The true impact of the pandemic on the job market will likely not be known until 2021 when many expect unemployment to peak.

However, as more is known, and the continued uncertainty prevails, governments are likely to continue to prop up economies which provides more optimistic outlooks for employment.

Job retention schemes in selected countries

Photo by Saulo Mohana on Unsplash