Momentum to gather in 2024

The Knight Frank UK Industrial and Logistics Market Update – Our monthly update on the UK industrial and logistics market, and expectations for the months ahead.

5 minutes to read

Latest OBR forecasts point to improved economic and fiscal outlook

Inflation is falling more quickly than previously expected. The OBR (Office for Budget Responsibility) March 2024 forecasts show their expectations of a sharp fall in inflation in 2024, with CPI expected to reach 2.2% by year-end, down from 7.3% at the end of 2023. The OBR expect the Bank of England to cut interest rates from the current base rate of 5.25% to 4.2% by the end of the year.

The steeper fall in inflation and interest rates will support a stronger recovery in output this year and next. The OBR have therefore revised up their GDP forecasts for this year, albeit modestly, with real GDP expected to rise 0.8% in 2024, compared with their previous forecast (November 2023) of 0.7% growth.

Lower inflation will support household income growth, with a quicker decline in inflation increasing the chances of a consumer-led recovery. Consumer spending grew just 0.3% in 2023, with negative growth of -1% recorded in the second half of the year.

Consumer rebound in 2024 and beyond should support an uptick in retailer demand

Online retailers were highly active in 2020/21 as they sought to rapidly scale up their distribution networks and capture a share of the rapidly expanding online shopping and home delivery market. During the Covid pandemic, online retail penetration rates reached a peak of 37.8% in January 2021. However, following the lifting of restrictions, they have since retreated. In January 2024, 26.3% of sales occurred online, down from 27.3% last January.

Retail occupiers have been far less acquisitive in terms of space over the past couple of years. Overall retail sales volumes (excluding automotive fuel) have shrunk in the past two years (Oxford Economics). However, positive growth is set to return in 2024, accelerating through 2025 and 2026. Growth in both online and physical retail sales should support growth in demand from retail occupiers.

Occupier market on the right track

There have been some sizeable take-up transactions so far this year, signalling improving sentiment from occupiers. While we don't expect a return to the frenzied levels of network expansion witnessed during Covid, we anticipate continued growth in demand to come from a range of occupier groups, particularly third-party logistics firms (3PLs). Companies are increasingly outsourcing their logistics and distribution activities to 3PL providers with specialist knowledge of efficiently managing inventory, deliveries, and returns.

The largest occupier transaction so far this year involves 3PL Yusen Logistics, who signed a pre-let agreement for 1.2 million sq ft at SEGRO Logistics Park Northampton. The building will become the largest facility operated by Yusen worldwide, enabling them to provide customers with rail freight distribution due to links to the Strategic Rail Freight Interchange. Online homeware retailer Dusk have also recently taken space at a multi-modal scheme, iPort Doncaster, which has an on-site rail freight terminal with daily services to and from Southampton, Felixstowe and Teesport.

Rail freight produces significantly lower emissions than other modes, with each tonne of freight transported creating 76% fewer carbon emissions compared to road. Currently, one in four sea containers arriving at UK ports is carried inland by rail, but there are ambitions to grow this.

In February, the government announced the creation of a new public body to drive forward the UK's rail freight sector and has set a rail freight growth target of at least 75% growth by 2050. In England and Wales, the Office of Rail and Road has set an interim target of 7.5% growth by 2029, and in Scotland, an even more ambitious target growth rate of 8.7% has been set. In addition to new infrastructure, logistics facilities will be needed to support this modal shift.

Freight is also being shifted off roads on to waterways. In February, planning consent was granted for a new mixed-use, residential and logistics scheme on Wandsworth Bridge Road, which includes a new jetty to improve capacity for handling waterborne cargo. The scheme is set to provide a 55,000 sq ft logistics facility, alongside 276 apartments. Cargo boats will bring goods up the River Thames to dock in the scheme's ground-floor wharf, enabling them to be sustainably distributed across London. This will allow the expansion of waterborne freight distribution in London. DHL already has a well-established light parcel ferry service that operates on the Thames, bringing packages from London Heathrow to central and east London via a pier in the west, avoiding congestion and reducing emissions.

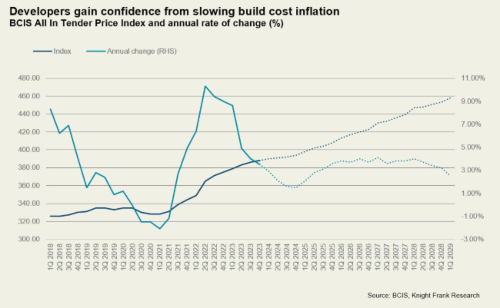

Developer confidence rising

Last year, heightened build and financing costs dampened construction activity. Though interest rates remain elevated and construction costs continue to rise, the rate of increase has slowed significantly. In Q1 2023, the BCIS All-In Tender Price Index rose 8.6% y/y, in Q1 2024 the annual rise is forecast to be around just 2.6%.

With greater certainty around pricing, developers are now more willing to commit. The number of construction starts in the first two months of this year is up significantly from last year, with 15 starts this year, compared with 8 in the same period last year.

Supply chain resilience and growth of the manufacturing sector remain high priorities

Ongoing attacks from Houthi rebels in the Red Sea are impacting trade via the Suez Canal shipping route that connects the UK and Europe with China and East Asia. These disruptions have driven ships to take much longer routes, impacting lead times and shipping costs. They will also ensure continued focus on supply chain resilience and the need to expand domestic production. There have been numerous disruptions to supply chains in recent years, and manufacturers and logistics operators have become acutely aware of the risks and have sought to improve their supply chain resilience by holding additional stock, bolstering their domestic manufacturing capabilities or sourcing more components from domestic suppliers.

Our Future Gazing research (2024) found that an additional 33.8 million sq ft of industrial and logistics space will be needed by 2028 to accommodate the forecast growth in manufacturing output. The manufacturing sector is central to the government's economic growth strategy. In the Spring Budget 2024, Chancellor Jeremy Hunt announced a £270m investment package in the UK's advanced manufacturing sectors (automotive and aerospace R&D), which should help support this growth. The sector accounts for 43% of all UK exports and is, therefore, critical to the government's aim of reaching £1 trillion in exports by 2030, which will require growth of 20% compared with 2022 figures.